Portfolio Optimization and Asset Allocation

Quantitative investment managers and risk managers use portfolio optimization to choose the proportions of various assets to be held in a portfolio. The goal of portfolio optimization is to maximize a measure or proxy for a portfolio's return contingent on a measure or proxy for a portfolio’s risk. This toolbox provides a comprehensive suite of portfolio optimization and analysis tools for performing capital allocation, asset allocation, and risk assessment using mean-variance, Conditional Value-at-Risk (CVaR), Mean-Absolute Deviation (MAD), and custom portfolio optimizations. In addition, the toolbox provides a backtesting framework to backtest portfolio allocation strategies and performance attribution functions for single periods, over relatively short time spans, or multiple periods.

Frequently Viewed Topics

- Portfolio Optimization Theory

- Portfolio Object Workflow

- PortfolioCVaR Object Workflow

- PortfolioMAD Object Workflow

- Using Extreme Value Theory and Copula Fitting to Generate Synthetic Data

- Black-Litterman Portfolio Optimization Using Financial Toolbox

- When to Use Portfolio Objects Over Optimization Toolbox

- Portfolio Optimization Using Factor Models

- Asset Allocation Case Study

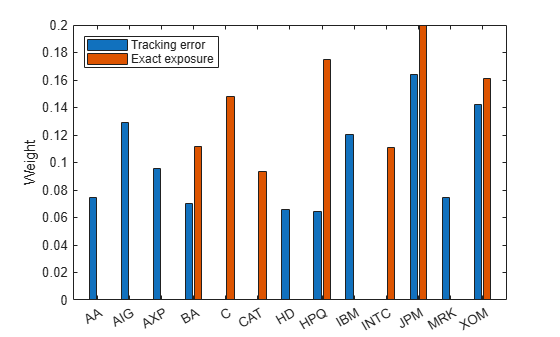

- Solve Tracking Error Portfolio Problems

- Risk Budgeting Portfolio

- Solve Problem for Minimum Tracking Error with Net Return Constraint

- Solve Robust Portfolio Maximum Return Problem with Ellipsoidal Uncertainty

- Hedging Using CVaR Portfolio Optimization

- Compute Maximum Reward-to-Risk Ratio for CVaR Portfolio

- Backtest with Brinson Attribution to Evaluate Portfolio Performance

- Choose MINLP Solvers for Portfolio Problems

- Troubleshooting Portfolio Optimization Results

Categories

- Portfolio Optimization Theory

Background theory for Portfolio optimization problems

- Mean-Variance Portfolio Optimization

Create Portfolio object, evaluate composition of assets, perform mean-variance portfolio optimization

- Conditional Value-at-Risk Portfolio Optimization

Create PortfolioCVaR object, evaluate composition of assets, perform CVaR portfolio optimization

- Mean-Absolute Deviation Portfolio Optimization

Create PortfolioMAD object, evaluate composition of assets, perform MAD portfolio optimization

- Custom Portfolio Optimization

Estimate optimal portfolio, specify user-defined objective function, define constraints

- Portfolio Analysis

Analyze portfolio for returns variance and covariance, simulate correlation of assets, calculate portfolio value at risk (VaR)

- Backtest Framework

Define investment strategies, run backtests, analyze strategy performance

- Performance Attribution

Compute and analyze performance attribution using the Brinson model

Featured Examples

Portfolio Optimization Examples Using Financial Toolbox

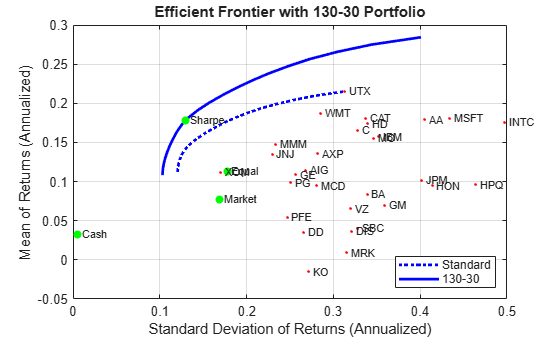

Follow a sequence of examples that highlight features of the Portfolio object. Specifically, the examples use the Portfolio object to show how to set up mean-variance portfolio optimization problems that focus on the two-fund theorem, the impact of transaction costs and turnover constraints, how to obtain portfolios that maximize the Sharpe ratio, and how to set up two popular hedge-fund strategies — dollar-neutral and 130-30 portfolios.

Portfolio Optimization Against a Benchmark

Demonstrates optimizing a portfolio to maximize the information ratio relative to a market benchmark.

Backtest Investment Strategies Using Financial Toolbox

Perform backtesting of portfolio strategies using a backtesting framework. Backtesting is a useful tool to compare how investment strategies perform over historical or simulated market data. This example develops five different investment strategies and then compares their performance after running over a one-year period of historical stock data. The backtesting framework is implemented in two Financial Toolbox™ classes: backtestStrategy and backtestEngine.

Backtest Investment Strategies with Trading Signals

Perform backtesting of portfolio strategies that incorporate investment signals in their trading strategy. The term signals includes any information that a strategy author needs to make with respect to trading decisions outside of the price history of the assets. Such information can include technical indicators, the outputs of machine learning models, sentiment data, macroeconomic data, and so on. This example uses three simple investment strategies based on derivative signal data:

Backtest Strategies Using Deep Learning

Construct trading strategies using a deep learning model and then backtest the strategies using the Financial Toolbox™ backtesting framework. The example uses Deep Learning Toolbox™ to train a predictive model from a set of time series and demonstrates the steps necessary to convert the model output into trading signals. It builds a variety of trading strategies that backtest the signal data over a 5-year period.

Backtest Deep Learning Model for Algorithmic Trading of Limit Order Book Data

Apply a backtest strategy to measure the performance of a long short-term memory (LSTM) neural network, which is trained and validated on limit order book (LOB) data of a security.

Portfolio Optimization Using Social Performance Measure

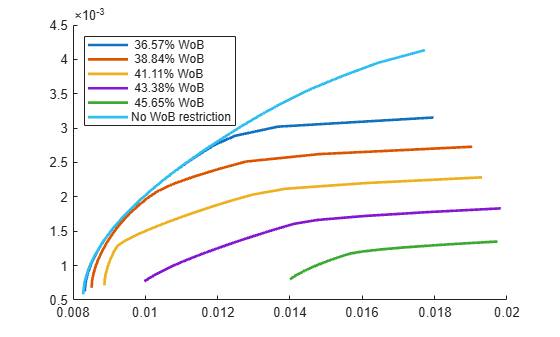

Use a Portfolio object to minimize the variance, maximize return, and maximize the average percentage of women on a company's board. The same workflow can be applied with other Environmental, Social and Governance (ESG) criteria, such as an ESG score, a climate, or a temperature score.

Diversify ESG Portfolios

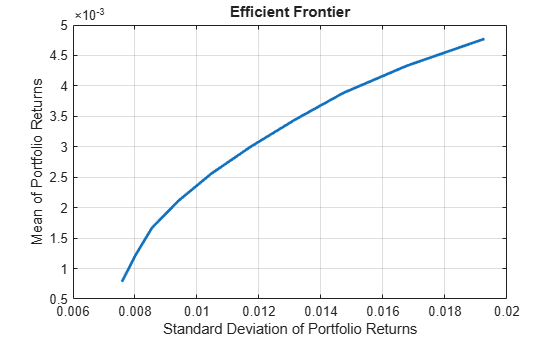

Include qualitative factors for environmental, social, and corporate governance (ESG) in the portfolio selection process. The example extends the traditional mean-variance portfolio using a Portfolio object to include the ESG metric. First, the estimateFrontier function computes the mean-variance efficient frontier for different ESG levels. Then, the example illustrates how to combine the ESG performance measure with portfolio diversification techniques. Specifically, it introduces hybrid models that use the Herfindahl-Hirshman (HH) index and the most diversified portfolio (MDP) approach using the estimateCustomObjectivePortfolio function. Finally, the backtestEngine framework compares the returns and behavior of the different ESG strategies.

Backtest Using Risk-Based Equity Indexation

Use backtesting with a risk parity or equal risk contribution strategy rebalanced approximately every month as a risk-based indexation. In this example, you use the backtesting engine (backtestEngine) to create the risk parity strategy, that all assets in the portfolio contribute equally to the risk of the portfolio at each rebalancing period.

Create Hierarchical Risk Parity Portfolio

Compute a hierarchical risk parity (HRP) portfolio. You can use HRP as a technique for portfolio diversification where the assets are divided and weighted according to a hierarchical tree structure. The weights of the assets within a cluster and between clusters can be assigned in many ways. A few ideas of the ways to allocate the weights are:

Bond Portfolio Optimization Using Portfolio Object

Use a Portfolio object to construct an optimal portfolio of 10, 20, and 30 year treasuries that will be held for a period of one month. The workflow for the overall asset allocation process is:

Analyze Performance Attribution Using Brinson Model

Prepare data, create a brinsonAttribution object, and then analyze the performance attribution with respect to category (sector) weights and returns. In this example, you use the categoryAttribution, categoryReturns, categoryWeights, totalAttribution, and summary functions for the analysis. Also, you can generate plots for the results, using categoryReturnsChart, categoryWeightsChart, and attributionsChart.

Diversify Portfolios Using Custom Objective

Three techniques of asset diversification in a portfolio using the estimateCustomObjectivePortfolio function with a Portfolio object. The purpose of asset diversification is to balance the exposure of the portfolio to any given asset to reduce volatility over a period of time. Given the sensitivity of the minimum variance portfolio to the estimation of the covariance matrix, some practitioners have added diversification techniques to the portfolio selection with the hope of minimizing risk measures other than the variance measures such as turnover, maximum drawdown, and so on.

Single Period Goal-Based Wealth Management

A method for goal-based wealth management (GBWM). In GBWM, risk is not necessarily measured using the standard deviation, the value-at-risk, or any other common risk measure. Instead, risk is understood as the likelihood of not attaining an investor's goal. You choose a weight allocation that is on the traditional mean-variance efficient frontier and that also maximizes the probability of exceeding a wealth goal at the end of the investment horizon. In other words, you choose the portfolio on the efficient frontier that minimizes the risk of not attaining the investor's goal.

Dynamic Portfolio Allocation in Goal-Based Wealth Management for Multiple Time Periods

A dynamic programming strategy to maximize the probability of obtaining an investor's wealth goal at the end of the investment horizon. This dynamic programming strategy is known in the literature as a goal-based wealth management (GBWM) strategy. In GBWM, risk is not necessarily measured using the standard deviation, the value-at-risk, or any other common risk metric. Instead, risk is understood as the likelihood of not attaining an investor's goal. This alternative concept of risk implies that, sometimes, in order to increase the probability of attaining an investor’s goal, the optimal portfolio’s traditional risk (that is, standard deviation) must increase if the portfolio is underfunded. In other words, for the investor’s view of risk to decrease, the traditional view of risk must increase if the portfolio’s wealth is too low.

Multiperiod Goal-Based Wealth Management Using Reinforcement Learning

A reinforcement learning (RL) approach to maximize the probability of obtaining an investor's wealth goal at the end of the investment horizon. This problem is known in the literature as goal-based wealth management (GBWM). In GBWM, risk is not necessarily measured using the standard deviation, the value-at-risk, or any other common risk metric. Instead, risk is understood as the likelihood of not attaining an investor's goal. This alternative concept of risk implies that, sometimes, in order to increase the probability of attaining an investor’s goal, the optimal portfolio’s traditional risk (that is, standard deviation) must increase if the portfolio is underfunded. In other words, for the investor’s view of risk to decrease, the traditional view of risk must increase if the portfolio’s wealth is too low.

Compare Performance of Covariance Denoising with Factor Modeling Using Backtesting

Uses backtesting to compare the performance of two investment strategies that use factor information to compute the portfolio weights. The first investment strategy uses covarianceDenoising to estimate both the covariance matrix and the number of factors to use in the second investment strategy. The second investment strategy uses a principal component analysis (PCA) factor model to estimate the covariance matrix with the number of factors obtained with covarianceDenoising. The PCA factor model follows the process in Portfolio Optimization Using Factor Models.

Deep Reinforcement Learning for Optimal Trade Execution

Use the Reinforcement Learning Toolbox™ and Deep Learning Toolbox™ to design agents for optimal trade execution.

Mixed-Integer Mean-Variance Portfolio Optimization Problem

Solve a mean-variance portfolio optimization problem with constraints in the number of selected assets or conditional (semicontinuous) bounds. To solve this problem, you can use a Portfolio object along with different mixed integer nonlinear programming (MINLP) solvers.

Optimize Portfolio Using Fama-French Model

Compare two approaches to optimize a portfolio with multiple risk factors. Both approaches use the Fama-French three-factor model to estimate risk in terms of size, value, and the overall return of the market.