Troubleshooting Portfolio Optimization Results

Remove warnings from loading preR2026a Portfolio, PortfolioCVaR, and PortfolioMAD objects

When you load portfolio objects from a

MAT-file saved in a previous MATLAB version (R2025b or earlier), you get various

warnings because the intlinprog

"legacy" algorithm has been removed. One such warning is:

Warning: Error caught while loading option Algorithm. Ignoring saved

value. (since R2026a)

To remove the warnings, do one of the following:

Resave the portfolio object to a new MAT-file. For example, after loading your portfolio object P from an older MAT-file, resave it as follows:

save("ResavedPortfolio","P");

The outcome is that all

Portfoliosolver options are set to the current defaults, replacing any obsolete settings with those newly-supported options for the"HiGHS"algorithm.Remove the options

IntMainSolverOptions,CutSelectionHeuristicandQuantileThresholdand recreate a new object usingsetSolverMINLPas follows.solverOptions = P.solverOptionsMINLP; solverOptions = rmfield(solverOptions,["IntMainSolverOptions",... "CutSelectionHeuristic","QuantileThreshold"]); P = setSolverMINLP(P,P.solverTypeMINLP,solverOptions); save("AlternativePortfolio.mat","P");

Portfolio Object Destroyed When Modifying

If a Portfolio object is destroyed when modifying, remember to

pass an existing object into the Portfolio object if you want to

modify it, otherwise it creates a new object. See Creating the Portfolio Object for details.

Optimization Fails with “Bad Pivot” Message

If the optimization fails with a "bad pivot" message from

lcprog, try a larger value for tolpiv

which is a tolerance for pivot selection in the lcprog algorithm

(try 1.0e-7, for example) or try the

interior-point-convex version of quadprog. For details, see Choosing and Controlling the Solver for Mean-Variance Portfolio Optimization, the help header for

lcprog, and quadprog.

Speed of Optimization

Although it is difficult to characterize when one algorithm is faster than the

other, the default solver, quadprog solver is faster for larger

problems and lcprog is faster for smaller problems. If one solver

seems to take too much time, try the other solver. To change solvers, use setSolver.

Matrix Incompatibility and "Non-Conformable" Errors

If you get matrix incompatibility or "non-conformable" errors, the representation of data in the tools follows a specific set of basic rules described in Conventions for Representation of Data.

Missing Data Estimation Fails

If asset return data has missing or NaN values, the estimateAssetMoments function with

the 'missingdata' flag set to true may fail

with either too many iterations or a singular covariance. To correct this problem,

consider this:

If you have asset return data with no missing or

NaNvalues, you can compute a covariance matrix that may be singular without difficulties. If you have missing orNaNvalues in your data, the supported missing data feature requires that your covariance matrix must be positive-definite, that is, nonsingular.estimateAssetMomentsuses default settings for the missing data estimation procedure that might not be appropriate for all problems.

In either case, you might want to estimate the moments of asset

returns separately with either the ECM estimation functions such as ecmnmle or with your own

functions.

mv_optim_transform Errors

If you obtain optimization errors such as:

Error using mv_optim_transform (line 233) Portfolio set appears to be either empty or unbounded. Check constraints. Error in Portfolio/estimateFrontier (line 63) [A, b, f0, f, H, g, lb] = mv_optim_transform(obj);

Error using mv_optim_transform (line 238) Cannot obtain finite lower bounds for specified portfolio set. Error in Portfolio/estimateFrontier (line 63) [A, b, f0, f, H, g, lb] = mv_optim_transform(obj);

estimateBounds to examine your

portfolio set, and use checkFeasibility to ensure that

your initial portfolio is either feasible and, if infeasible, that you have

sufficient turnover to get from your initial portfolio to the portfolio set.

Tip

To correct this problem, try solving your problem with larger values for turnover or tracking-error and gradually reduce to the value that you want.

solveContinuousCustomObjProb or solveMICustomObjProb Errors

These errors can occur if the portfolio set is empty or unbounded. If the

portfolio set is empty, the error states that the problem is infeasible. The best

way to deal with these problems is to use the validation functions in Validate the Portfolio Problem for Portfolio Object.

Specifically, use estimateBounds to examine your

portfolio set, and use checkFeasibility to ensure that

your initial portfolio is either feasible or, if infeasible, that you have

sufficient turnover to get from your initial portfolio to the portfolio set.

Efficient Portfolios Do Not Make Sense

If you obtain efficient portfolios that do not seem to make sense, this can happen

if you forget to set specific constraints or you set incorrect constraints. For

example, if you allow portfolio weights to fall between 0 and

1 and do not set a budget constraint, you can get portfolios

that are 100% invested in every asset. Although it may be hard to detect, the best

thing to do is to review the constraints you have set with display of the object. If

you get portfolios with 100% invested in each asset, you can review the display of

your object and quickly see that no budget constraint is set. Also, you can use

estimateBounds and checkFeasibility to determine if

the bounds for your portfolio set make sense and to determine if the portfolios you

obtained are feasible relative to an independent formulation of your portfolio

set.

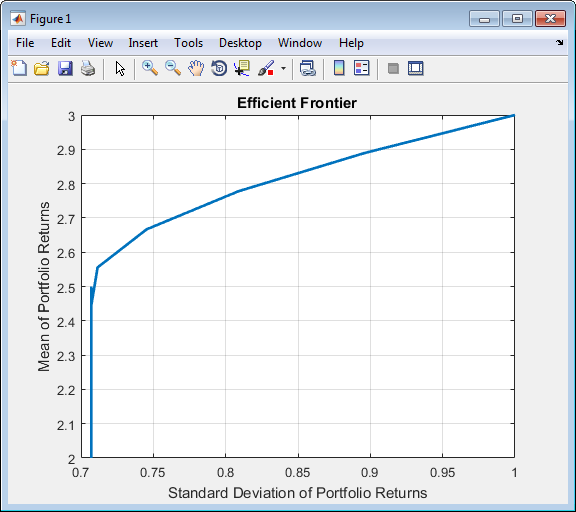

Efficient Frontiers Do Not Make Sense

If you obtain efficient frontiers that do not seem to make sense, this can happen

for some cases of mean and covariance of asset returns. It is possible for some

mean-variance portfolio optimization problems to have difficulties at the endpoints

of the efficient frontier. It is rare for standard portfolio problems, but this can

occur. For example, this can occur when using unusual combinations of turnover

constraints and transaction costs. Usually, the workaround of setting the hidden

property enforcePareto produces a single portfolio for the entire

efficient frontier, where any other solutions are not Pareto optimal (which is what

efficient portfolios must be).

An example of a portfolio optimization problem that has difficulties at the endpoints of the efficient frontier is this standard mean-variance portfolio problem (long-only with a budget constraint) with the following mean and covariance of asset returns:

m = [ 1; 2; 3 ]; C = [ 1 1 0; 1 1 0; 0 0 1 ]; p = Portfolio; p = Portfolio(p, 'assetmean', m, 'assetcovar', C); p = Portfolio(p, 'lowerbudget', 1, 'upperbudget', 1); p = Portfolio(p, 'lowerbound', 0); plotFrontier(p)

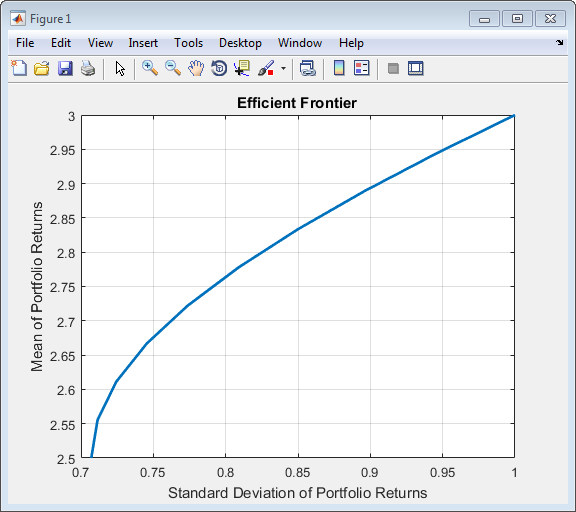

To work around this problem, set the hidden Portfolio object property for

enforcePareto. This property instructs the optimizer to

perform extra steps to ensure a Pareto-optimal solution. This slows down the solver,

but guarantees a Pareto-optimal solution.

p.enforcePareto = true; plotFrontier(p)

Troubleshooting estimateCustomObjectivePortfolio

When using estimateCustomObjectivePortfolio, nonconvex functions are not

supported for problems with cardinality constraints or conditional bounds.

Specifically, the following error displays when using estimateCustomObjectivePortfolio with a Portfolio object that includes

'Conditional'

BoundType (semicontinuous) constraints using setBounds or

MinNumAssets and MaxNumAssets

(cardinality) constraints using setMinMaxNumAssets.

Error using solveMICustomObjProb

Objective function must be convex in problems with cardinality constraints and/or conditional bounds.

Error in Portfolio/estimateCustomObjectivePortfolio (line 88)

[pwgt,exitflag] = solveMICustomObjProb(obj,prob,fun,flags);Note

This error applies only to quadratic functions. This error is not detected in nonlinear functions. Therefore, if you are using a nonlinear function, you must validate your input.

For more information, see Role of Convexity in Portfolio Problems.

Troubleshooting for Setting 'Conditional' BoundType, MinNumAssets, and MaxNumAssets Constraints

When configuring a Portfolio, PortfolioCVaR, or PortfolioMAD object to include

'Conditional'

BoundType (semicontinuous) constraints using setBounds or

MinNumAssets and MaxNumAssets

(cardinality) constraints using setMinMaxNumAssets, the values of the inputs that you supply can result

in warning messages.

Conditional Bounds with LowerBound Defined as Empty or Zero

When using setBounds with

the BoundType set to 'Conditional' and the

LowerBound input argument is empty ([

]) or 0, the Conditional

bound is not effective and is equivalent to a Simple

bound.

AssetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

AssetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

p = setBounds(p, 0, 0.5, 'BoundType', 'Conditional');

p = setMinMaxNumAssets(p, 3, 3);

estimateFrontier(p, 10)Warning: Conditional bounds with 'LowerBound' as zero are equivalent to simple bounds.

Consider either using strictly positive 'LowerBound' or 'simple' as the 'BoundType'

instead.

> In internal.finance.PortfolioMixedInteger/checkBoundType (line 46)

In Portfolio/checkarguments (line 204)

In Portfolio/setBounds (line 80)

Warning: The solution may have less than 'MinNumAssets' assets with nonzero weight. To

enforce 'MinNumAssets' requirement, set strictly positive lower conditional bounds.

> In internal.finance.PortfolioMixedInteger/hasIntegerConstraints (line 44)

In Portfolio/estimateFrontier (line 51)

ans =

Columns 1 through 8

0.5000 0.3555 0.3011 0.3299 0.3585 0.3873 0.4160 0.4448

0.5000 0.5000 0.4653 0.3987 0.3322 0.2655 0.1989 0.1323

0.0000 0.1445 0.2335 0.2714 0.3093 0.3472 0.3850 0.4229

Columns 9 through 10

0.4735 0.5000

0.0657 0

0.4608 0.5000In all the 10 optimal allocations, there are allocations (the first and last

ones) that only have two assets, which is in conflict with the

MinNumAssets constraint that three assets should be

allocated. Also there are two warnings, which actually explain what happens. In

this case, the 'Conditional' bound constraints are defined as

xi = 0 or 0 <=

xi <= 0.5, which are internally

modeled as

0*vi<=xi<=0.5*vi,

where vi is 0 or 1,

where 0 indicates not allocated, and 1

indicates allocated. Here, vi=1, which

still allows the asset to have a weight of 0. In other words,

setting LowerBound as 0 or empty, doesn’t

clearly define the minimum allocation for an allocated asset. Therefore, a

0 weighted asset is also considered as an allocated

asset. To fix this warning, follow the instructions in the warning message, and

set a LowerBound value that is strictly

positive.

AssetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

AssetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

p = setBounds(p, 0.3, 0.5, 'BoundType', 'Conditional');

p = setMinMaxNumAssets(p, 3, 3);

estimateFrontier(p, 10)ans =

Columns 1 through 8

0.3000 0.3180 0.3353 0.3489 0.3580 0.3638 0.3694 0.3576

0.4000 0.3820 0.3642 0.3479 0.3333 0.3199 0.3067 0.3001

0.3000 0.3000 0.3005 0.3032 0.3088 0.3163 0.3240 0.3423

Columns 9 through 10

0.3289 0.3000

0.3000 0.3000

0.3711 0.4000

Length of 'BoundType' Must Be Conformable with NumAssets

The setBounds

optional name-value argument for 'BoundType' must be defined

for all assets in a Portfolio, PortfolioCVaR, or PortfolioMAD object. By default,

the 'BoundType' is 'Simple' and applies to

all assets. Using setBounds, you

can choose to define a 'BoundType' for each asset. In this

case, the number of 'BoundType' specifications must match the

number of assets (NumAssets) in the Portfolio, PortfolioCVaR, or PortfolioMAD object. The

following example demonstrates the error when the number of

'BoundType' specifications do not match the number of

assets in the Portfolio

object.

AssetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

AssetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

p = setBounds(p, 0.1, 0.5, 'BoundType',["simple"; "conditional"])

Cannot create bound constraints.

Caused by:

Error using internal.finance.PortfolioMixedInteger/checkBoundType (line 28)

Length of 'BoundType' must be conformable with 'NumAssets'=3.To correct this, modify the BoundType to include three

specifications because the Portfolio object has three

assets.

AssetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

AssetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

p = setBounds(p, 0.1, 0.5, 'BoundType',["simple"; "conditional";"conditional"])

p.BoundTypep =

Portfolio with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

AssetMean: [3×1 double]

AssetCovar: [3×3 double]

TrackingError: []

TrackingPort: []

Turnover: []

BuyTurnover: []

SellTurnover: []

Name: []

NumAssets: 3

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [3×1 double]

UpperBound: [3×1 double]

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

BoundType: [3×1 categorical]

MinNumAssets: []

MaxNumAssets: []

ans =

3×1 categorical array

simple

conditional

conditional

Redundant Constraints from 'BoundType', 'MinNumAssets', 'MaxNumAssets' Constraints

When none of the constraints from 'BoundType',

'MinNumAssets', or 'MaxNumAssets' are

active, the redundant constraints from 'BoundType',

'MinNumAssets', 'MaxNumAssets' warning

occurs. This happens when you explicitly use setBounds and

setMinMaxNumAssets but with values that are inactive. That is,

the 'Conditional'

BoundType has a LowerBound = [

] or 0, 'MinNumAssets' is

0, or 'MaxNumAssets' is the same value

as NumAssets. In other words, if any of these three are

active, the warning will not show up when using the estimate

functions or plotFrontier. The following two

examples show the rationale.

The first example is when the BoundType is explicitly set

as 'Conditional' but the LowerBound is

0, and no 'MinNumAssets' and

'MaxNumAssets' constraints are defined using setMinMaxNumAssets.

AssetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

AssetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

p = setBounds(p, 0, 0.5, 'BoundType', 'Conditional');

estimateFrontier(p, 10)Warning: Redundant constraints from 'BoundType', 'MinNumAssets', 'MaxNumAssets'.

> In internal.finance.PortfolioMixedInteger/hasIntegerConstraints (line 24)

In Portfolio/estimateFrontier (line 51)

ans =

Columns 1 through 8

0.5000 0.3555 0.3011 0.3299 0.3586 0.3873 0.4160 0.4448

0.5000 0.5000 0.4653 0.3987 0.3321 0.2655 0.1989 0.1323

0 0.1445 0.2335 0.2714 0.3093 0.3471 0.3850 0.4229

Columns 9 through 10

0.4735 0.5000

0.0657 0

0.4608 0.5000The second example is when you explicitly set the three constraints, but all

with inactive values. In this example, the BoundType is

'Conditional' and the LowerBound is

0, thus specifying ineffective

'Conditional'

BoundType constraints, and the

'MinNumAssets' and 'MaxNumAssets'

values are 0 and 3, respectively. The

setMinMaxNumAssets function specifies ineffective

'MinNumAssets' and 'MaxNumAssets'

constraints.

AssetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

AssetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

p = setBounds(p, 0, 0.5, 'BoundType', 'Conditional');

p = setMinMaxNumAssets(p, 0, 3);

estimateFrontier(p, 10)Warning: Redundant constraints from 'BoundType', 'MinNumAssets', 'MaxNumAssets'.

> In internal.finance.PortfolioMixedInteger/hasIntegerConstraints (line 24)

In Portfolio/estimateFrontier (line 51)

ans =

Columns 1 through 8

0.5000 0.3555 0.3011 0.3299 0.3586 0.3873 0.4160 0.4448

0.5000 0.5000 0.4653 0.3987 0.3321 0.2655 0.1989 0.1323

0 0.1445 0.2335 0.2714 0.3093 0.3471 0.3850 0.4229

Columns 9 through 10

0.4735 0.5000

0.0657 0

0.4608 0.5000Infeasible Problem with Conditional (Semi-Continuous) Bounds, Cardinality Constraints, or Conditional Budget Constraints

The Portfolio, PortfolioCVaR, or PortfolioMAD object performs

validations of all the constraints before solving any specific optimization

problems. The Portfolio, PortfolioCVaR, or

PortfolioMAD object first considers all constraints other

than conditional bounds, cardinality constraints, and conditional budget

constraints and issues an error message if they are not compatible. Then the

Portfolio, PortfolioCVaR, or

PortfolioMAD object adds the remaining constraints to

check if they are compatible with the already checked constraints. This

separation is natural because conditional bounds, cardinality constraints, and

conditional budget constraints require additional binary variables in the

mathematical formulation that leads to an MINLP, while other constraints only

need continuous variables. You can follow the error messages to check when the

infeasible problem occurs and take actions to fix the constraints.

One possible scenario is when the BoundType is

'Conditional' and Groups are defined for the

Portfolio object. In this case, the Group definitions are

themselves in conflict. Consequently, the 'Conditional' bound

constraint cannot be applied when running estimateFrontierLimits.

AssetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

AssetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

p = setBounds(p, 0.1, 0.5, 'BoundType','Conditional');

p = setGroups(p, [1,1,0], 0.3, 0.5);

p = addGroups(p, [0,1,0], 0.6, 0.7);

pwgt = estimateFrontierLimits(p)Error using Portfolio/buildMixedIntegerProblem (line 31)

Infeasible problem prior to considering constraints involving integer variables.

Verify compatibility of continuous constraints.

Error in Portfolio/estimateFrontierLimits>int_frontierLimits (line 93)

ProbStruct = buildMixedIntegerProblem(obj);

Error in Portfolio/estimateFrontierLimits (line 73)

pwgt = int_frontierLimits(obj, minsolution, maxsolution);To correct this error, change the LowerGroup in the

addGroups function to also be

0.3 to match the GroupMatrix input

from setGroups.

AssetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

AssetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

p = setBounds(p, 0.1, 0.5, 'BoundType','Conditional');

p = setGroups(p, [1,1,0], 0.3, 0.5);

p = addGroups(p, [0,1,0], 0.3, 0.7);

pwgt = estimateFrontierLimits(p)

pwgt =

0 0.2000

0.5000 0.3000

0.5000 0.5000A second possible scenario is when the BoundType is

'Conditional' and the setEquality function is used

with the bEquality parameter set to 0.04.

This sets an equality constraint to have x1 +

x3 = 0.04. At the same time, setBounds also

set the semicontinuous constraints to have xi =

0 or 0.1 <= xi

<= 2.5, which lead to x1 +

x3 = 0 or 0.1 <=

x1 + x3 <= 5.

The semicontinuous constraints are not compatible with the equality constraint

because there is no way to get x1 + x3 to

equal 0.04. Therefore, the error message is

displayed.

AssetMean = [ 0.05; 0.1; 0.12; 0.18 ];

AssetCovar = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

A = [ 1 0 1 0 ];

b = 0.04;

p = setEquality(p, A, b);

p = setBounds(p, 0.1, 2.5, 'BoundType','Conditional');

p = setMinMaxNumAssets(p, 2, 2);

pwgt = estimateFrontierLimits(p)Error using Portfolio/buildMixedIntegerProblem (line 109)

Infeasible problem when considering constraints involving integer variables.

Verify constraints compatibility or decrease 'AbsoluteGapTolerance' or 'RelativeGapTolerance'.

Error in Portfolio/estimateFrontierLimits>int_frontierLimits (line 93)

ProbStruct = buildMixedIntegerProblem(obj);

Error in Portfolio/estimateFrontierLimits (line 73)

pwgt = int_frontierLimits(obj, minsolution, maxsolution);

To correct this error, change the bEquality parameter from

0.04 to .4.

AssetMean = [ 0.05; 0.1; 0.12; 0.18 ];

AssetCovar = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar, 'Budget', 1);

A = [ 1 0 1 0 ];

b = 0.4;

p = setEquality(p, A, b);

p = setBounds(p, 0.1, 2.5, 'BoundType','Conditional');

p = setMinMaxNumAssets(p, 2, 2);

pwgt = estimateFrontierLimits(p)pwgt =

0.4000 0

0.6000 0

0 0.4000

0 0.6000Redundant Conditional Budget Constraint

This redundant conditional budget constraint warning occurs when you are using

setConditionalBudget with a Portfolio, PortfolioCVaR, or PortfolioMAD object and the

conditional threshold of all assets is greater than or equal to their respective

upper bounds. This happens when the UpperBound ≤

ConditionalBudgetThreshold. In this case, assets are not

allowed to invest more than the conditional threshold, which makes the

conditional budget constraint unnecessary. The following example shows the case

where this

happens:

assetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

assetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio(AssetMean=assetMean,AssetCovar=assetCovar);

p = setBounds(p,0,0.5);

p = setConditionalBudget(p,0.5,0.75);

estimateFrontier(p)

Warning: Redundant conditional budget constraint.

> In internal.finance.PortfolioMixedInteger/hasIntegerConstraints (line 59)

In Portfolio/estimateFrontier (line 54)

ans =

0 0.0454 0.0909 0.1825 0.3186 0.4547 0.5000 0.5000 0.5000 0.5000

0 0.2008 0.4015 0.5000 0.5000 0.5000 0.5000 0.5000 0.5000 0.5000

0 0.0169 0.0338 0.0491 0.0629 0.0766 0.1574 0.2716 0.3858 0.5000To correct this warning, use setBounds to

specify an UpperBound value that is > than the

ConditionalBudgetThreshold that you specify using

setConditionalBudget.

assetMean = [ 0.0101110; 0.0043532; 0.0137058 ];

assetCovar = [ 0.00324625 0.00022983 0.00420395;

0.00022983 0.00049937 0.00019247;

0.00420395 0.00019247 0.00764097 ];

p = Portfolio(AssetMean=assetMean,AssetCovar=assetCovar);

p = setBounds(p,0,0.55);

p = setConditionalBudget(p,0.5,0.75);

estimateFrontier(p)

ans =

0.0000 0.0477 0.0953 0.1799 0.3226 0.4653 0.5000 0.5000 0.5000 0.5000

0.0001 0.2107 0.4212 0.5500 0.5500 0.5500 0.5500 0.5500 0.5500 0.5000

0.0000 0.0177 0.0355 0.0519 0.0663 0.0808 0.1749 0.2947 0.4144 0.5500

Unbounded Portfolio Problem

This error occurs when you are using a Portfolio, PortfolioCVaR, or PortfolioMAD object and there is

no UpperBound defined in setBounds and

you are using setMinMaxNumAssets. In this case, this is formulated as a mixed

integer programming problem and an UpperBound is required to

enforce MinNumAssets and MaxNumAssets

constraints.

The optimizer first attempts to estimate the upper bound of each asset, based

on all the specified constraints. If the UpperBound cannot be

found, an error message occurs which instructs you to set an explicit

UpperBound. In most cases, as long as you set some upper

bounds to the problem using any set function, the optimizer

can successfully find a good

estimation.

AssetMean = [ 0.05; 0.1; 0.12; 0.18 ];

AssetCovar = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar);

p = setBounds(p, 0.1, 'BoundType','Conditional');

p = setGroups(p, [1,1,1,0], 0.3, 0.5);

p = setMinMaxNumAssets(p, 3, 3);

pwgt = estimateFrontierLimits(p)Error using Portfolio/buildMixedIntegerProblem (line 42)

Unbounded portfolio problem. Upper bounds cannot be inferred from the existing

constraints. Set finite upper bounds using 'setBounds'.

Error in Portfolio/estimateFrontierLimits>int_frontierLimits (line 93)

ProbStruct = buildMixedIntegerProblem(obj);

Error in Portfolio/estimateFrontierLimits (line 73)

pwgt = int_frontierLimits(obj, minsolution, maxsolution);To correct this error, specify an UpperBound value for

setBounds.

AssetMean = [ 0.05; 0.1; 0.12; 0.18 ];

AssetCovar = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

p = Portfolio('AssetMean', AssetMean, 'AssetCovar', AssetCovar);

p = setBounds(p, 0.1, .9, 'BoundType','Conditional');

p = setGroups(p, [1,1,1,0], 0.3, 0.5);

p = setMinMaxNumAssets(p, 3, 3);

pwgt = estimateFrontierLimits(p)pwgt =

0.1000 0

0.1000 0.1000

0.1000 0.4000

0 0.9000Total Number of Portfolio Weights with a Value > 0 Are Greater Than MaxNumAssets Specified

When using a Portfolio, PortfolioCVaR, or PortfolioMAD object, the optimal

allocation w may contain some very small values that leads to

sum(w>0) larger

than MaxNumAssets, even though the

MaxNumAssets constraint is specified using setMinMaxNumAssets. For example, in the following code when

setMinMaxNumAssets is used to set

MaxNumAssets to 15, the

sum(w>0) indicates

that there are 19 assets. A close examination of the weights

shows that the weights are extremely small and are actually

0.

T = readtable('dowPortfolio.xlsx'); symbol = T.Properties.VariableNames(3:end); assetReturn = tick2ret(T{:,3:end}); p = Portfolio('AssetList', symbol, 'budget', 1); p = setMinMaxNumAssets(p, 10, 15); p = estimateAssetMoments(p,assetReturn); p = setBounds(p,0.01,0.5,'BoundType','Conditional','NumAssets',30); p = setTrackingError(p,0.05,ones(1, p.NumAssets)/p.NumAssets); w = estimateFrontierLimits(p,'min'); % minimum risk portfolio sum(w>0) % Number of assets that are allocated in the optimal portfolio w(w<eps) % Check the weights of the very small weighted assets

ans =

19

ans =

1.0e-20 *

-0.0000

0

0

0.0293

0

0.3626

0.2494

0

0.0926

-0.0000

0

0.0020

0

0

0

0

This situation only happens when the OuterApproximation

algorithm is used with setSolverMINLP to

solve a MINLP portfolio optimization problem. The

OuterApproximation internally fixes the latest solved

integer variables and runs an NLP with quadprog or fmincon, which introduces numerical

issues and leads to weights that are very close to 0.

If you do not want to deal with very small values, you can use setSolverMINLP to

select a different algorithm. In this example, the

'TrustRegionCP' algorithm is

specified.

T = readtable('dowPortfolio.xlsx'); symbol = T.Properties.VariableNames(3:end); assetReturn = tick2ret(T{:,3:end}); p = Portfolio('AssetList', symbol, 'budget', 1); p = setMinMaxNumAssets(p, 10, 15); p = estimateAssetMoments(p,assetReturn); p = setBounds(p,0.01,0.5,'BoundType','Conditional','NumAssets',30); p = setTrackingError(p,0.05,ones(1, p.NumAssets)/p.NumAssets); p = setSolverMINLP(p,'TrustRegionCP'); w = estimateFrontierLimits(p,'min'); % minimum risk portfolio sum(w>0) % Number of assets that are allocated in the optimal portfolio w(w<eps) % The weights of the very small weighted assets are strictly zeros

ans =

14

ans =

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

See Also

Portfolio | estimateAssetMoments | checkFeasibility | setBounds | setMinMaxNumAssets

Topics

- Postprocessing Results to Set Up Tradable Portfolios

- Creating the Portfolio Object

- Working with Portfolio Constraints Using Defaults

- Estimate Efficient Portfolios for Entire Efficient Frontier for Portfolio Object

- Estimate Efficient Frontiers for Portfolio Object

- Asset Allocation Case Study

- Portfolio Optimization Examples Using Financial Toolbox

- Portfolio Optimization with Semicontinuous and Cardinality Constraints

- Black-Litterman Portfolio Optimization Using Financial Toolbox

- Portfolio Optimization Using Factor Models

- Portfolio Optimization Using Social Performance Measure

- Diversify Portfolios Using Custom Objective

- Troubleshooting CVaR Portfolio Optimization Results

- Troubleshooting MAD Portfolio Optimization Results

- Portfolio Object

- Portfolio Optimization Theory

- Portfolio Object Workflow