Model Seasonal Lag Effects Using Indicator Variables

This example shows how to estimate a seasonal ARIMA model:

Model the seasonal effects using a multiplicative seasonal model.

Use indicator variables as a regression component for the seasonal effects, called seasonal dummies.

Subsequently, their forecasts show that the methods produce similar results. The time series is monthly international airline passenger numbers from 1949 to 1960.

Load Data

Load the data set Data_Airline, and plot the natural log of the monthly passenger totals counts.

load Data_Airline dat = log(DataTimeTable.PSSG); % Transform to logarithmic scale T = size(dat,1); y = dat(1:103); % Estimation sample

y is the part of dat used for estimation, and the rest of dat is the holdout sample to compare the two models' forecasts.

Fit Seasonal-Lag Model

Create an ARIMA model

where is an independent and identically distributed normally distributed series with mean 0 and variance . Use estimate to fit Mdl1 to y.

Mdl1 = arima('Constant',0,'MALags',1,'D',1,... 'SMALags',12,'Seasonality',12); EstMdl1 = estimate(Mdl1,y);

ARIMA(0,1,1) Model Seasonally Integrated with Seasonal MA(12) (Gaussian Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ __________

Constant 0 0 NaN NaN

MA{1} -0.35732 0.088031 -4.059 4.9286e-05

SMA{12} -0.61469 0.096249 -6.3864 1.6985e-10

Variance 0.001305 0.0001527 8.5467 1.2671e-17

The fitted model is

where is an iid normally distributed series with mean 0 and variance 0.0013.

Fit Seasonal-Dummy Model

Create an ARIMAX(0,1,1) model with period 12 seasonal differencing and a regression component,

is a series of T column vectors having length 12 that indicate in which month observation was measured. A 1 in row i of indicates that the observation was measured in month i, the rest of the elements are 0s.

Note that if you include an additive constant in the model, then the T rows of the design matrix X are composed of the row vectors . Therefore, X is rank deficient, and one regression coefficient is not identifiable. A constant is left out of this example to avoid distraction from the main purpose. Format the in-sample X matrix

X = dummyvar(repmat((1:12)',12,1)); % Format the presample X matrix X0 = [zeros(1,11) 1; dummyvar((1:12)')]; Mdl2 = arima('Constant',0,'MALags',1,'D',1,... 'Seasonality',12); EstMdl2 = estimate(Mdl2,y,'X',[X0; X]);

ARIMAX(0,1,1) Model Seasonally Integrated (Gaussian Distribution):

Value StandardError TStatistic PValue

__________ _____________ __________ __________

Constant 0 0 NaN NaN

MA{1} -0.40711 0.084387 -4.8242 1.4053e-06

Beta(1) -0.002577 0.025168 -0.10239 0.91845

Beta(2) -0.0057769 0.031885 -0.18118 0.85623

Beta(3) -0.0022034 0.030527 -0.072179 0.94246

Beta(4) 0.00094737 0.019867 0.047687 0.96197

Beta(5) -0.0012146 0.017981 -0.067551 0.94614

Beta(6) 0.00487 0.018374 0.26505 0.79097

Beta(7) -0.0087944 0.015285 -0.57535 0.56505

Beta(8) 0.0048346 0.012484 0.38728 0.69855

Beta(9) 0.001437 0.018245 0.078758 0.93722

Beta(10) 0.009274 0.014751 0.62869 0.52955

Beta(11) 0.0073665 0.0105 0.70158 0.48294

Beta(12) 0.00098841 0.014295 0.069146 0.94487

Variance 0.0017715 0.00024657 7.1848 6.7329e-13

The fitted model is

where is an iid normally distributed series with mean 0 and variance 0.0017 and is a column vector with the values Beta1 - Beta12. Note that the estimates MA{1} and Variance between Mdl1 and Mdl2 are not equal.

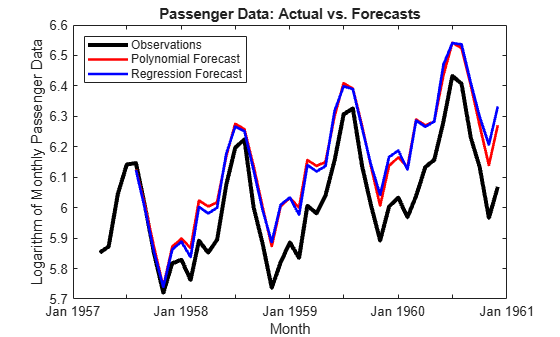

Forecast Both Models

Use forecast to forecast both models 41 periods into the future from July 1957. Plot the holdout sample using these forecasts.

fT = 41; fh = DataTimeTable.Time((end-fT+1):end); yF1 = forecast(EstMdl1,41,y); yF2 = forecast(EstMdl2,41,y,'X0',X(1:103,:),'XF',X(104:end,:)); l1 = plot(DataTimeTable.Time(100:end),dat(100:end),'k','LineWidth',3); hold on l2 = plot(fh,yF1,'-r','LineWidth',2); l3 = plot(fh,yF2,'-b','LineWidth',2); hold off title('Passenger Data: Actual vs. Forecasts') xlabel('Month') ylabel('Logarithm of Monthly Passenger Data') legend({'Observations','Polynomial Forecast',... 'Regression Forecast'},'Location','NorthWest')

Though they overpredict the holdout observations, the forecasts of both models are almost equivalent. One main difference between the models is that EstMdl1 is more parsimonious than EstMdl2.

References:

Box, G. E. P., G. M. Jenkins, and G. C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

See Also

Objects

Functions

Topics

- Create Seasonal ARIMA (SARIMA) Model for Time Series Data

- Estimate Seasonal ARIMA (SARIMA) Model

- Forecast Multiplicative ARIMA Model

- Check Fit of Multiplicative ARIMA Model

- Forecast IGD Rate from ARX Model

- Create Seasonal ARIMA (SARIMA) Models

- Create ARIMA Models That Include Exogenous Covariates

- Conditional Mean Model Estimation with Equality Constraints

- Forecast Conditional Mean Model Programmatically