predictLifetime

Compute cumulative lifetime PD, marginal PD, and survival probability

Syntax

Description

LifeTimePredictedPD = predictLifetime(pdModel,data)

LifeTimePredictedPD = predictLifetime(___,Name,Value)

Examples

This example shows how to use fitLifetimePDModel to fit data with a Probit model and then predict the lifetime probability of default (PD).

Load Data

Load the credit portfolio data.

load RetailCreditPanelData.mat

disp(head(data)) ID ScoreGroup YOB Default Year

__ __________ ___ _______ ____

1 Low Risk 1 0 1997

1 Low Risk 2 0 1998

1 Low Risk 3 0 1999

1 Low Risk 4 0 2000

1 Low Risk 5 0 2001

1 Low Risk 6 0 2002

1 Low Risk 7 0 2003

1 Low Risk 8 0 2004

disp(head(dataMacro))

Year GDP Market

____ _____ ______

1997 2.72 7.61

1998 3.57 26.24

1999 2.86 18.1

2000 2.43 3.19

2001 1.26 -10.51

2002 -0.59 -22.95

2003 0.63 2.78

2004 1.85 9.48

Join the two data components into a single data set.

data = join(data,dataMacro); disp(head(data))

ID ScoreGroup YOB Default Year GDP Market

__ __________ ___ _______ ____ _____ ______

1 Low Risk 1 0 1997 2.72 7.61

1 Low Risk 2 0 1998 3.57 26.24

1 Low Risk 3 0 1999 2.86 18.1

1 Low Risk 4 0 2000 2.43 3.19

1 Low Risk 5 0 2001 1.26 -10.51

1 Low Risk 6 0 2002 -0.59 -22.95

1 Low Risk 7 0 2003 0.63 2.78

1 Low Risk 8 0 2004 1.85 9.48

Partition Data

Separate the data into training and test partitions.

nIDs = max(data.ID); uniqueIDs = unique(data.ID); rng('default'); % for reproducibility c = cvpartition(nIDs,'HoldOut',0.4); TrainIDInd = training(c); TestIDInd = test(c); TrainDataInd = ismember(data.ID,uniqueIDs(TrainIDInd)); TestDataInd = ismember(data.ID,uniqueIDs(TestIDInd));

Create a Probit Lifetime PD Model

Use fitLifetimePDModel to create a Probit model using the training data.

pdModel = fitLifetimePDModel(data(TrainDataInd,:),"Probit",... 'AgeVar','YOB',... 'IDVar','ID',... 'LoanVars','ScoreGroup',... 'MacroVars',{'GDP','Market'},... 'ResponseVar','Default'); disp(pdModel)

Probit with properties:

ModelID: "Probit"

Description: ""

UnderlyingModel: [1×1 classreg.regr.CompactGeneralizedLinearModel]

IDVar: "ID"

AgeVar: "YOB"

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: 1

Display the underlying model.

disp(pdModel.Model)

Compact generalized linear regression model:

probit(Default) ~ 1 + ScoreGroup + YOB + GDP + Market

Distribution = Binomial

Estimated Coefficients:

Estimate SE tStat pValue

__________ _________ _______ ___________

(Intercept) -1.6267 0.03811 -42.685 0

ScoreGroup_Medium Risk -0.26542 0.01419 -18.704 4.5503e-78

ScoreGroup_Low Risk -0.46794 0.016364 -28.595 7.775e-180

YOB -0.11421 0.0049724 -22.969 9.6208e-117

GDP -0.041537 0.014807 -2.8052 0.0050291

Market -0.0029609 0.0010618 -2.7885 0.0052954

388097 observations, 388091 error degrees of freedom

Dispersion: 1

Chi^2-statistic vs. constant model: 1.85e+03, p-value = 0

Predict Lifetime PD on Training and Test Data

Use the predictLifetime function to get lifetime PDs on the training or the test data. To get conditional PDs, use the predict function. For model validation, use the modelDiscrimination and modelCalibration functions on the training or test data.

DataSetChoice ="Testing"; if DataSetChoice=="Training" Ind = TrainDataInd; else Ind = TestDataInd; end % Predict lifetime PD PD = predictLifetime(pdModel,data(Ind,:)); head(data(Ind,:))

ID ScoreGroup YOB Default Year GDP Market

__ ___________ ___ _______ ____ _____ ______

2 Medium Risk 1 0 1997 2.72 7.61

2 Medium Risk 2 0 1998 3.57 26.24

2 Medium Risk 3 0 1999 2.86 18.1

2 Medium Risk 4 0 2000 2.43 3.19

2 Medium Risk 5 0 2001 1.26 -10.51

2 Medium Risk 6 0 2002 -0.59 -22.95

2 Medium Risk 7 0 2003 0.63 2.78

2 Medium Risk 8 0 2004 1.85 9.48

Predict Lifetime PD on New Data

Lifetime PD models are used to make predictions on existing loans. The predictLifetime function requires projected values for both the loan and macro predictors for the remainder of the life of the loan.

The DataPredictLifetime.mat file contains projections for two loans and also for the macro variables. One loan is three years old at the end of 2019, with a lifetime of 10 years, and the other loan is six years old with a lifetime of 10 years. The ScoreGroup is constant and the age values are incremental. For the macro variables, the forecasts for the macro predictors must span the longest lifetime in the portfolio.

load DataPredictLifetime.mat

disp(LoanData) ID ScoreGroup YOB Year

____ _____________ ___ ____

1304 "Medium Risk" 4 2020

1304 "Medium Risk" 5 2021

1304 "Medium Risk" 6 2022

1304 "Medium Risk" 7 2023

1304 "Medium Risk" 8 2024

1304 "Medium Risk" 9 2025

1304 "Medium Risk" 10 2026

2067 "Low Risk" 7 2020

2067 "Low Risk" 8 2021

2067 "Low Risk" 9 2022

2067 "Low Risk" 10 2023

disp(MacroScenario)

Year GDP Market

____ ___ ______

2020 1.1 4.5

2021 0.9 1.5

2022 1.2 5

2023 1.4 5.5

2024 1.6 6

2025 1.8 6.5

2026 1.8 6.5

2027 1.8 6.5

LifetimeData = join(LoanData,MacroScenario); disp(LifetimeData)

ID ScoreGroup YOB Year GDP Market

____ _____________ ___ ____ ___ ______

1304 "Medium Risk" 4 2020 1.1 4.5

1304 "Medium Risk" 5 2021 0.9 1.5

1304 "Medium Risk" 6 2022 1.2 5

1304 "Medium Risk" 7 2023 1.4 5.5

1304 "Medium Risk" 8 2024 1.6 6

1304 "Medium Risk" 9 2025 1.8 6.5

1304 "Medium Risk" 10 2026 1.8 6.5

2067 "Low Risk" 7 2020 1.1 4.5

2067 "Low Risk" 8 2021 0.9 1.5

2067 "Low Risk" 9 2022 1.2 5

2067 "Low Risk" 10 2023 1.4 5.5

Predict lifetime PDs and store the output as a new table column for convenience.

LifetimeData.PredictedPD = predictLifetime(pdModel,LifetimeData); disp(LifetimeData)

ID ScoreGroup YOB Year GDP Market PredictedPD

____ _____________ ___ ____ ___ ______ ___________

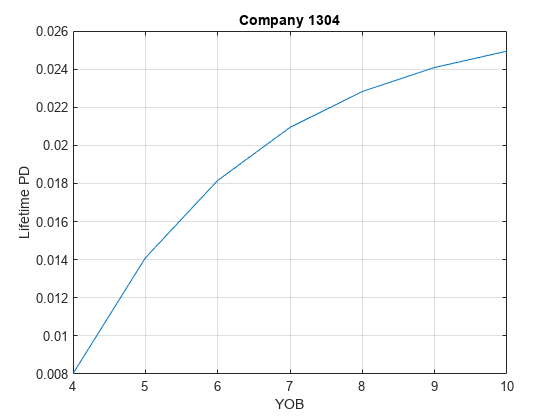

1304 "Medium Risk" 4 2020 1.1 4.5 0.0080202

1304 "Medium Risk" 5 2021 0.9 1.5 0.014093

1304 "Medium Risk" 6 2022 1.2 5 0.018156

1304 "Medium Risk" 7 2023 1.4 5.5 0.020941

1304 "Medium Risk" 8 2024 1.6 6 0.022827

1304 "Medium Risk" 9 2025 1.8 6.5 0.024086

1304 "Medium Risk" 10 2026 1.8 6.5 0.024945

2067 "Low Risk" 7 2020 1.1 4.5 0.0015728

2067 "Low Risk" 8 2021 0.9 1.5 0.0027146

2067 "Low Risk" 9 2022 1.2 5 0.003431

2067 "Low Risk" 10 2023 1.4 5.5 0.0038939

Visualize the predicted lifetime PD for a company.

CompanyIDChoice ="1304"; CompanyID = str2double(CompanyIDChoice); IndPlot = LifetimeData.ID==CompanyID; plot(LifetimeData.YOB(IndPlot),LifetimeData.PredictedPD(IndPlot)) grid on xlabel('YOB') xticks(LifetimeData.YOB(IndPlot)) ylabel('Lifetime PD') title(strcat("Company ",CompanyIDChoice))

This example shows how time interval plays an important role for lifetime prediction when using a Logistic, Probit, Cox, or customLifetimePDModel model for probability of default (PD).

As described in predictLifetime, each PD value is a probability of default for the given time interval (for example, a time interval of 1 year). The data rows passed in for lifetime prediction must have the same periodicity as the time interval. In other words, you can't pass a row that represents a quarter, and then a row that represents a year, and then one that represents 5 years. You must pass data for periods 1, 2, 3, 4,..., but not 1, 3, 7, 10, 20. Or if the time interval is 3, you must pass periods 3, 6, 9,... or 2, 5, 8,..., but not 3, 7, 15, 30.

Fit Different Models

In this section, we fit three different models with different specifications:

A model with an age variable and with a time interval value estimated by

fitLifetimePDModelA model with no age variable

A custom model with age variable, but where the time interval is not specified

The behavior of the data validation in predictLifetime depends on the model type. For more information, see Validation of Data Input for Lifetime Prediction.

load RetailCreditPanelData.mat

data = join(data,dataMacro);

head(data) ID ScoreGroup YOB Default Year GDP Market

__ __________ ___ _______ ____ _____ ______

1 Low Risk 1 0 1997 2.72 7.61

1 Low Risk 2 0 1998 3.57 26.24

1 Low Risk 3 0 1999 2.86 18.1

1 Low Risk 4 0 2000 2.43 3.19

1 Low Risk 5 0 2001 1.26 -10.51

1 Low Risk 6 0 2002 -0.59 -22.95

1 Low Risk 7 0 2003 0.63 2.78

1 Low Risk 8 0 2004 1.85 9.48

Model with Age and Time Interval

Cox, Logistic, and Probit models estimate the time interval as long as a numeric variable is specified as age variable. customLifetimePDModel models support arguments to specify an age variable and time interval. Here, the model type can be selected to train a Cox, Logistic, or Probit model with age variable and let the fitLifetimePDModel estimate the time interval. For this data set, the time interval 1.

ModelType ="cox"; pdModelAgeAndTime = fitLifetimePDModel(data,ModelType,... 'ModelID','Age and Time Model','Description','Lifetime PD model with age and time interval',... 'IDVar','ID','AgeVar','YOB',... 'LoanVars','ScoreGroup','MacroVars',{'GDP' 'Market'},... 'ResponseVar','Default'); disp(pdModelAgeAndTime)

Cox with properties:

ExtrapolationFactor: 1

ModelID: "Age and Time Model"

Description: "Lifetime PD model with age and time interval"

UnderlyingModel: [1×1 CoxModel]

IDVar: "ID"

AgeVar: "YOB"

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: 1

Models with age and time interval are the best situation. The time interval provides information on the periodicity of the PD predictions, and it also allows predictLifetime to validate the periodicity of the data input for lifetime prediction, as shown in the last section of this example.

Model with No Age

For Cox models, the age information is required. For Logistic and Probit models, the age variable is optional, although it is a common predictor for lifetime PD models. For illustration purposes, here we estimate a Logistic or Probit model without age variable.

The fitLifetimePDModel function is unable to estimate the time interval because this is estimated based on age increments. See Time Interval for Logistic Models and Time Interval for Probit Models for more information.

ModelType ="logistic"; pdModelNoAge = fitLifetimePDModel(data,ModelType,... 'ModelID','No Age Model','Description','Lifetime PD model without age',... 'IDVar','ID',... 'LoanVars','ScoreGroup','MacroVars',{'GDP' 'Market'},... 'ResponseVar','Default'); disp(pdModelNoAge)

Logistic with properties:

ModelID: "No Age Model"

Description: "Lifetime PD model without age"

UnderlyingModel: [1×1 classreg.regr.CompactGeneralizedLinearModel]

IDVar: "ID"

AgeVar: ""

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: []

Note that a time interval could still be specified using the TimeInterval optional argument. This may still be valuable information to specify to store as meta data in the TimeInterval property of the model. However, because there is no age variable, the predictLifetime function would still be unable to validate the periodicity of the data input for lifetime prediction.

Model Without Time Interval

There are some situations where a lifetime PD model object may have an empty TimeInterval property, such as a custom model where no time interval was specified when creating the model instance with customLifetimePDModel.

sc = creditscorecard(data,'IDVar','ID',... 'PredictorVars',{'ScoreGroup' 'YOB' 'GDP' 'Market'},... 'ResponseVar','Default'); sc = autobinning(sc); sc = autobinning(sc,'YOB','Algorithm','Split'); sc = fitmodel(sc,'Display','off'); displaypoints(sc)

ans=16×3 table

Predictors Bin Points

______________ _______________ _______

{'ScoreGroup'} {'High Risk' } 0.61102

{'ScoreGroup'} {'Medium Risk'} 1.3043

{'ScoreGroup'} {'Low Risk' } 1.9113

{'ScoreGroup'} {'<missing>' } NaN

{'YOB' } {'[-Inf,2)' } 0.56226

{'YOB' } {'[2,5)' } 1.0024

{'YOB' } {'[5,7)' } 1.4549

{'YOB' } {'[7,Inf]' } 2.509

{'YOB' } {'<missing>' } NaN

{'GDP' } {'[-Inf,0.63)'} 1.042

{'GDP' } {'[0.63,Inf]' } 1.1657

{'GDP' } {'<missing>' } NaN

{'Market' } {'[-Inf,2.78)'} 1.0731

{'Market' } {'[2.78,9.48)'} 1.1219

{'Market' } {'[9.48,Inf]' } 1.2294

{'Market' } {'<missing>' } NaN

pdFcnHandle = @(data) probdefault(sc,data); pdModelNoTime = customLifetimePDModel(pdFcnHandle,IDVar='ID',... AgeVar='YOB',Description='Scorecard as lifetime PD model',... LoanVars='ScoreGroup',MacroVars={'GDP' 'Market'},... ModelID='ScorecardLifetime',ResponseVar='Default'); disp(pdModelNoTime)

CustomLifetimePD with properties:

ModelID: "ScorecardLifetime"

Description: "Scorecard as lifetime PD model"

UnderlyingModel: @(data)probdefault(sc,data)

IDVar: "ID"

AgeVar: "YOB"

LoanVars: "ScoreGroup"

MacroVars: ["GDP" "Market"]

ResponseVar: "Default"

WeightsVar: ""

TimeInterval: []

In these situations, even if a numeric age variable is specified, the validation of the periodicity in the data input to predictLifetime is limited, because the model does not have a reference time interval to compare against. This is further discussed in the last section of this example.

Conditional PD and Model Validation

The conditional PD values returned by predict are consistent with the time interval used for training the model. In this example, all PD values returned by predict are 1-year probabilities of default. There is no validation of the periodicity in the data input for predict. The PD prediction is a row-by-row operation, the rows are processed independently, regardless of their ID or periodicity. For illustration purposes, pick a few random rows from the original data and call the predict method, and verify that any of the above models works without warnings or errors.

dataPredictExample = data([1 2 6 10 15],:); ModelChoice ="Age and Time Interval"; switch ModelChoice case "Age and Time Interval" pdModel = pdModelAgeAndTime; case "No Age" pdModel = pdModelNoAge; case "No Time Interval" pdModel = pdModelNoTime; end pdExample = predict(pdModel,dataPredictExample)

pdExample = 5×1

0.0089

0.0052

0.0038

0.0094

0.0031

Model validation is done using the conditional PD returned by predict. Therefore, there is no row periodicity validation in modelDiscrimination or modelCalibration. However, model validation requires observed values of the response variable, and the definition of default used for the validation response values must be consistent with the training data. In other words, if the training data uses a time interval of 1, the validation response data cannot be defined with quarterly default data. There are no row-periodicity checks for modelDiscrimination or modelCalibration, it is assumed that the default definition in the validation data is consistent with the training data.

modelCalibrationPlot(pdModel,data,{'YOB','ScoreGroup'})

Lifetime PD

The predictLifetime function is used to compute lifetime PD. When making lifetime predictions:

A different data set is likely used, not the data you used for training and validation, but a new data set with forward-looking projections for different loans.

The projected values in the lifetime prediction data set span several periods ahead, potentially several years ahead.

Load the DataPredictLifetime.mat data for lifetime prediction. Note that for prediction, you don't need to pass the response data, you only pass predictors. You only pass response values for fitting or validation, not for prediction.

load DataPredictLifetime.mat

LifetimeData = join(LoanData,MacroScenario);

disp(LifetimeData) ID ScoreGroup YOB Year GDP Market

____ _____________ ___ ____ ___ ______

1304 "Medium Risk" 4 2020 1.1 4.5

1304 "Medium Risk" 5 2021 0.9 1.5

1304 "Medium Risk" 6 2022 1.2 5

1304 "Medium Risk" 7 2023 1.4 5.5

1304 "Medium Risk" 8 2024 1.6 6

1304 "Medium Risk" 9 2025 1.8 6.5

1304 "Medium Risk" 10 2026 1.8 6.5

2067 "Low Risk" 7 2020 1.1 4.5

2067 "Low Risk" 8 2021 0.9 1.5

2067 "Low Risk" 9 2022 1.2 5

2067 "Low Risk" 10 2023 1.4 5.5

The rows have yearly data, consistent with the time interval used for training. You can see this in both the Year variable and the YOB variable. There are no flags in this data set for lifetime predictions.

ModelChoice ="Age and Time Interval"; switch ModelChoice case "Age and Time Interval" pdModel = pdModelAgeAndTime; case "No Age" pdModel = pdModelNoAge; case "No Time Interval" pdModel = pdModelNoTime; end LifetimeData.PD = predict(pdModel,LifetimeData); LifetimeData.LifetimePD = predictLifetime(pdModel,LifetimeData)

LifetimeData=11×8 table

ID ScoreGroup YOB Year GDP Market PD LifetimePD

____ _____________ ___ ____ ___ ______ __________ __________

1304 "Medium Risk" 4 2020 1.1 4.5 0.0081336 0.0081336

1304 "Medium Risk" 5 2021 0.9 1.5 0.0063861 0.014468

1304 "Medium Risk" 6 2022 1.2 5 0.0047416 0.019141

1304 "Medium Risk" 7 2023 1.4 5.5 0.0028262 0.021913

1304 "Medium Risk" 8 2024 1.6 6 0.0014844 0.023365

1304 "Medium Risk" 9 2025 1.8 6.5 0.0014517 0.024783

1304 "Medium Risk" 10 2026 1.8 6.5 0.0014517 0.026198

2067 "Low Risk" 7 2020 1.1 4.5 0.0016091 0.0016091

2067 "Low Risk" 8 2021 0.9 1.5 0.0009006 0.0025082

2067 "Low Risk" 9 2022 1.2 5 0.00085273 0.0033588

2067 "Low Risk" 10 2023 1.4 5.5 0.00083391 0.0041899

When the periodicity of the rows does not match the periodicity in the training data, the lifetime PD values cannot be correctly computed.

Modify the selected rows using the SelectedRows variable in the code to see the behavior of predictLifetime as the periodicity of the data changes. (Alternatively, the YOB values can be manually modified to enter age increments inconsistent with the time interval of 1 year.)

RowSelection ="All rows"; switch RowSelection case "All rows" SelectedRows = 1:11; % Selecting all rows 1:11 is the same as the output above, no warnings case "Every other row" SelectedRows = 1:2:11; % Regular age increments, but skipping one year case "Irregular" SelectedRows = [1 2 7 8 11]; % Irregular age increments end LifetimeData2 = LifetimeData(SelectedRows,{'ID','ScoreGroup','YOB','Year','GDP','Market'}); disp(LifetimeData2)

ID ScoreGroup YOB Year GDP Market

____ _____________ ___ ____ ___ ______

1304 "Medium Risk" 4 2020 1.1 4.5

1304 "Medium Risk" 5 2021 0.9 1.5

1304 "Medium Risk" 6 2022 1.2 5

1304 "Medium Risk" 7 2023 1.4 5.5

1304 "Medium Risk" 8 2024 1.6 6

1304 "Medium Risk" 9 2025 1.8 6.5

1304 "Medium Risk" 10 2026 1.8 6.5

2067 "Low Risk" 7 2020 1.1 4.5

2067 "Low Risk" 8 2021 0.9 1.5

2067 "Low Risk" 9 2022 1.2 5

2067 "Low Risk" 10 2023 1.4 5.5

Switch the trained model to see the behavior for different model specifications.

ModelChoice ="Age and Time Interval"; switch ModelChoice case "Age and Time Interval" pdModel = pdModelAgeAndTime; case "No Age" pdModel = pdModelNoAge; case "No Time Interval" pdModel = pdModelNoTime; end LifetimeData2.PD = predict(pdModel,LifetimeData2); LifetimeData2.LifetimePD = predictLifetime(pdModel,LifetimeData2); disp(LifetimeData2)

ID ScoreGroup YOB Year GDP Market PD LifetimePD

____ _____________ ___ ____ ___ ______ __________ __________

1304 "Medium Risk" 4 2020 1.1 4.5 0.0081336 0.0081336

1304 "Medium Risk" 5 2021 0.9 1.5 0.0063861 0.014468

1304 "Medium Risk" 6 2022 1.2 5 0.0047416 0.019141

1304 "Medium Risk" 7 2023 1.4 5.5 0.0028262 0.021913

1304 "Medium Risk" 8 2024 1.6 6 0.0014844 0.023365

1304 "Medium Risk" 9 2025 1.8 6.5 0.0014517 0.024783

1304 "Medium Risk" 10 2026 1.8 6.5 0.0014517 0.026198

2067 "Low Risk" 7 2020 1.1 4.5 0.0016091 0.0016091

2067 "Low Risk" 8 2021 0.9 1.5 0.0009006 0.0025082

2067 "Low Risk" 9 2022 1.2 5 0.00085273 0.0033588

2067 "Low Risk" 10 2023 1.4 5.5 0.00083391 0.0041899

As mentioned earlier, the most robust situation is when both the age variable and the time interval are specified in the lifetime PD model, because the tool can validate the periodicity of the data input. For cases without age information or without time interval information, only partial validation, and some times no validation, can be performed. In these cases, the predictLifetime function cannot distinguish between valid data inputs and invalid ones, so it performs the computations assuming the periodicity is correct to support cases with valid periodicity. The user is responsible for verifying that the periodicity of the data input is valid, especially when the age or time interval information are not available. For more information, see Validation of Data Input for Lifetime Prediction.

Input Arguments

Name-Value Arguments

Output Arguments

More About

References

[1] Baesens, Bart, Daniel Roesch, and Harald Scheule. Credit Risk Analytics: Measurement Techniques, Applications, and Examples in SAS. Wiley, 2016.

[2] Bellini, Tiziano. IFRS 9 and CECL Credit Risk Modelling and Validation: A Practical Guide with Examples Worked in R and SAS. San Diego, CA: Elsevier, 2019.

[3] Breeden, Joseph. Living with CECL: The Modeling Dictionary. Santa Fe, NM: Prescient Models LLC, 2018.

[4] Roesch, Daniel and Harald Scheule. Deep Credit Risk: Machine Learning with Python. Independently published, 2020.

Version History

Introduced in R2020bSee Also

predict | modelDiscrimination | modelDiscriminationPlot | modelCalibration | modelCalibrationPlot | fitLifetimePDModel | Logistic | Probit | Cox | customLifetimePDModel

Topics

- Basic Lifetime PD Model Validation

- Compare Logistic Model for Lifetime PD to Champion Model

- Compare Lifetime PD Models Using Cross-Validation

- Expected Credit Loss Computation

- Compare Model Discrimination and Model Calibration to Validate of Probability of Default

- Compare Probability of Default Using Through-the-Cycle and Point-in-Time Models

- Create Custom Lifetime PD Model for Decision Tree Model with Function Handle

- Overview of Lifetime Probability of Default Models