fitSmithWilson

Syntax

Description

outCurve = fitSmithWilson(Settle,Instruments,CleanPrice,UltimateForwardRate,LastLiquidPoint)parametercurve object.. After

creating a parametercurve object for outCurve, you

can use the associated object functions discountfactors,

zerorates, and

forwardrates.

outCurve = fitSmithWilson(___Name=Value)

Examples

Define the bond data and use fininstrument to create a FixedBond instrument object.

Settle = datetime("15-Jun-2023"); Maturity = Settle + calyears([2 4 6 9 18 30]'); CleanPrice = [100.1;100.1;100.8;96.6;103.3;96.3]; CouponRate = [0.0400;0.0425;0.0450;0.0400;0.0500;0.0425]; Bonds = fininstrument("FixedBond",Maturity=Maturity,CouponRate=CouponRate)

Bonds=6×1 FixedBond array with properties:

CouponRate

Period

Basis

EndMonthRule

Principal

DaycountAdjustedCashFlow

BusinessDayConvention

Holidays

IssueDate

FirstCouponDate

LastCouponDate

StartDate

Maturity

Name

Use fitSmithWilson to create a parametercurve object.

UltimateForwardRate = .042; LastLiquidPoint = 20; SW = fitSmithWilson(Settle,Bonds,CleanPrice,UltimateForwardRate,LastLiquidPoint,Basis=4)

SW =

parametercurve with properties:

Type: "discount"

Settle: 15-Jun-2023

Compounding: -1

Basis: 4

FunctionHandle: @(t)W(u_cf,t(:)')'*CF'*zeta+exp(-ultFwdInt*t(:))

Parameters: 0.1317

You can use the parametercurve object (SW) to compute discountfactors, zerorates, and forwardrates.

outDiscountFactors=discountfactors(SW,[datetime("15-Jun-2024");datetime("15-Jun-2027")])

outDiscountFactors = 2×1

0.9627

0.8456

outZeroRates = zerorates(SW,[datetime("15-Jun-2024");datetime("15-Jun-2027")])

outZeroRates = 2×1

0.0380

0.0419

outForwardRates = forwardrates(SW,datetime("15-Jun-2024"),datetime("15-Jun-2027"))

outForwardRates = 0.0432

Define the bond market data and use bndyield to compute the raw yield to maturity.

Settle = datetime("15-Jun-2023");

Maturity = Settle + calyears([2 4 6 9 18 30]');

CleanPrice = [100.1;100.1;100.8;96.6;103.3;96.3];

CouponRate = [0.0400;0.0425;0.0450;0.0400;0.0500;0.0425];

YTM = bndyield(CleanPrice,CouponRate,Settle,Maturity)YTM = 6×1

0.0395

0.0422

0.0435

0.0446

0.0473

0.0448

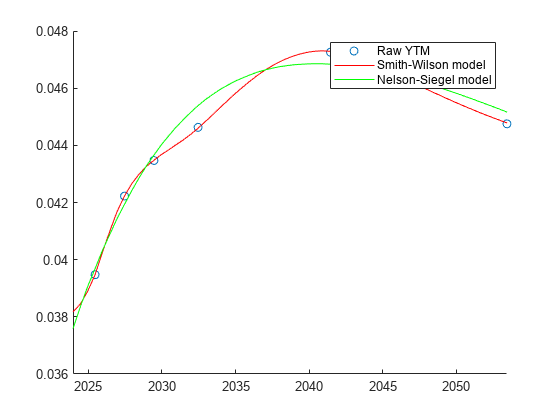

scatter(Maturity,YTM)

Use fininstrument to create a FixedBond instrument object using the bond data.

Bonds = fininstrument("FixedBond",Maturity=Maturity,CouponRate=CouponRate);Use fitSmithWilson to create a parametercurve object.

UltimateForwardRate = .033; LastLiquidPoint = 20; SW = fitSmithWilson(Settle,Bonds,CleanPrice,UltimateForwardRate,LastLiquidPoint)

SW =

parametercurve with properties:

Type: "discount"

Settle: 15-Jun-2023

Compounding: -1

Basis: 3

FunctionHandle: @(t)W(u_cf,t(:)')'*CF'*zeta+exp(-ultFwdInt*t(:))

Parameters: 0.0613

Use fitNelsonSiegel to create a parametercurve object.

NS = fitNelsonSiegel(Settle, Bonds, CleanPrice)

Local minimum possible. lsqnonlin stopped because the final change in the sum of squares relative to its initial value is less than the value of the function tolerance. <stopping criteria details>

NS =

parametercurve with properties:

Type: "zero"

Settle: 15-Jun-2023

Compounding: -1

Basis: 0

FunctionHandle: @(t)fitF(Params,t)

Parameters: [6.7223e-08 0.0363 0.0904 16.5171]

Plot a comparison of the fit of a Smith-Wilson model to a Nelson-Siegel model for the bond market data.

hold on PlottingTimes = calmonths(6:6:12*30)'; PlottingDates = Settle + PlottingTimes; PY_SW = zero2pyld(zerorates(SW,PlottingDates),PlottingDates,Settle,'InputCompounding',-1,'InputBasis',3,'OutputCompounding',2); PY_NS = zero2pyld(zerorates(NS,PlottingDates),PlottingDates,Settle,'InputCompounding',-1,'InputBasis',3,'OutputCompounding',2); plot(PlottingDates,PY_SW,'r') plot(PlottingDates,PY_NS,'g') legend(["Raw YTM","Smith-Wilson model","Nelson-Siegel model"])

Input Arguments

Name-Value Arguments

Output Arguments

More About

References

[1] Lagerås A., and M. Lindholm. "Issues with Smith-Wilson Method." Insurance: Mathematics and Economics. Vol. 71, 2016, pp. 93–102.

[2] Smith, A., and T. Wilson. "Fitting Yield Curves with Long Term Constraints." Research report, Bacon and Woodrow, 2000.

Version History

Introduced in R2024a