infer

Infer conditional variances of conditional variance models

Description

Tbl2 = infer(Mdl,Tbl1)Tbl2 containing the inferred

conditional variances and innovations from evaluating the fully specified,

univariate conditional variance model Mdl at the response

variable data in the table or timetable Tbl1. When

Mdl is a model fitted to the response data and returned by

estimate, the inferred innovations are

residuals. (since R2023a)

infer selects the response variable named in

Mdl.SeriesName or the sole variable in

Tbl1. To select a different response variable in

Tbl1 at which to evaluate the model, use the

ResponseVariable name-value argument.

___

= infer(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name,Value)infer returns the output argument combination for the

corresponding input arguments. For example, infer(Mdl,Y,V0=v0) initializes the

conditional variance model of Mdl using the presample

conditional variance data in v0.

Examples

Infer conditional variances from a GARCH(1,1) model with known coefficients. Specify response data as a numeric vector.

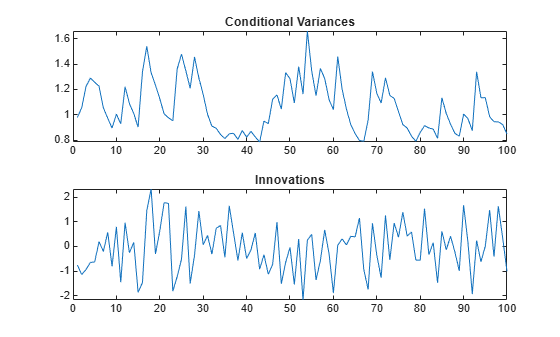

Specify a GARCH(1,1) model with known parameters. Simulate 101 conditional variances and responses (innovations) from the model. Set aside the first observation from each series to use as presample data.

Mdl = garch(Constant=0.01,GARCH=0.8,ARCH=0.15); rng(1,"twister") % For reproducibility [vS,yS] = simulate(Mdl,101); y0 = yS(1); v0 = vS(1); y = yS(2:end); v = vS(2:end); figure tiledlayout(2,1) nexttile plot(v) title("Conditional Variances") nexttile plot(y) title("Innovations")

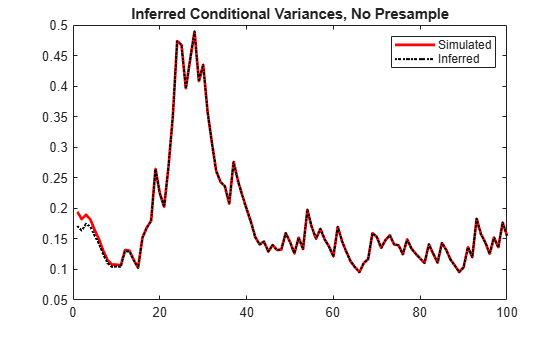

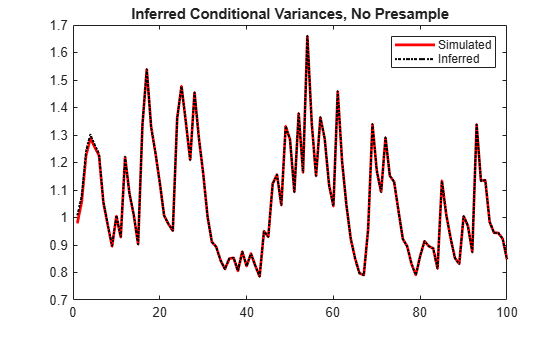

Infer the conditional variances of y without using presample data. Compare them to the known (simulated) conditional variances.

vI = infer(Mdl,y); figure plot(1:100,v,"r",LineWidth=2) hold on plot(1:100,vI,"k:",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, No Presample") hold off

Notice the transient response (discrepancy) in the early time periods due to the absence of presample data.

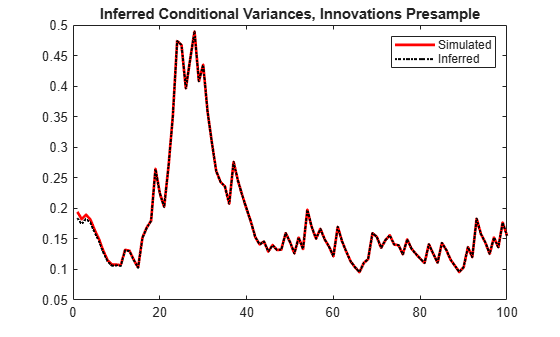

Infer conditional variances using the set-aside presample innovation, y0. Compare them to the known (simulated) conditional variances.

vE = infer(Mdl,y,E0=y0); figure plot(1:100,v,"r",LineWidth=2) hold on plot(1:100,vE,"k:",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Innovations Presample") hold off

There is a slightly reduced transient response in the early time periods.

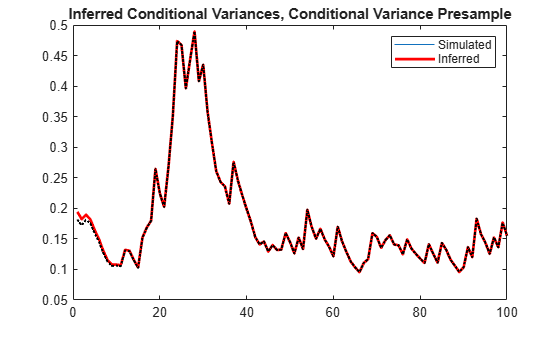

Infer conditional variances using the presample of conditional variance data, v0. Compare them to the known (simulated) conditional variances.

vO = infer(Mdl,y,V0=v0); figure plot(v) hold on plot(1:100,v,"r",LineWidth=2) plot(1:100,vO,"k:",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Conditional Variance Presample") hold off

There is a much smaller transient response in the early time periods.

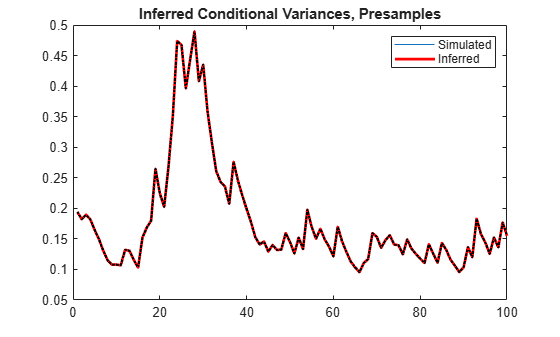

Infer conditional variances using both the presample innovation and conditional variance. Compare them to the known (simulated) conditional variances.

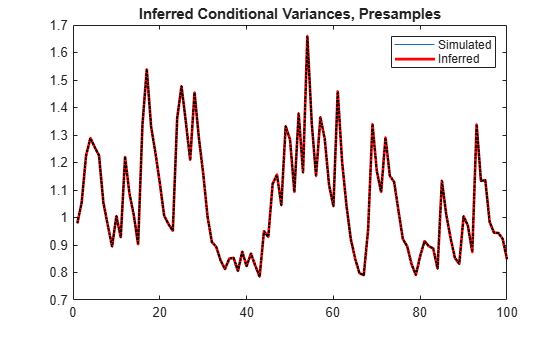

vEO = infer(Mdl,y,E0=y0,V0=v0); figure plot(v) hold on plot(1:100,v,"r",LineWidth=2) plot(1:100,vEO,"k:",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Presamples") hold off

When you use sufficient presample innovations and conditional variances, the inferred conditional variances are exact (there is no transient response).

Infer conditional variances from an EGARCH(1,1) model with known coefficients. When you use, and then do not use presample data, compare the results from infer.

Specify an EGARCH(1,1) model with known parameters. Simulate 101 conditional variances and responses (innovations) from the model. Set aside the first observation from each series to use as presample data.

Mdl = egarch(Constant=0.001,GARCH=0.8, ... ARCH=0.15,Leverage=-0.1); rng(1,"twister") % For reproducibility [vS,yS] = simulate(Mdl,101); y0 = yS(1); v0 = vS(1); y = yS(2:end); v = vS(2:end); figure tiledlayout(2,1) nexttile plot(v) title("Conditional Variances") nexttile plot(y) title("Innovations")

Infer the conditional variances of y without using any presample data. Compare them to the known (simulated) conditional variances.

vI = infer(Mdl,y); figure plot(1:100,v,"r",LineWidth=2) hold on plot(1:100,vI,"k:",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, No Presample") hold off

Notice the transient response (discrepancy) in the early time periods due to the absence of presample data.

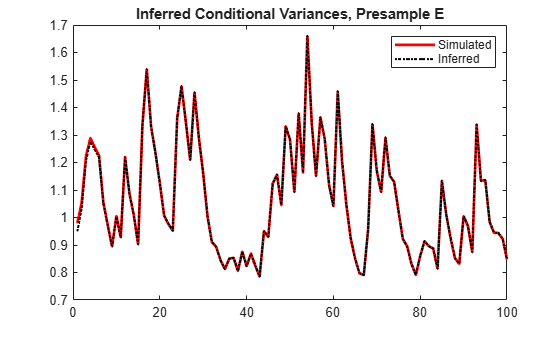

Infer conditional variances using the set-aside presample innovation, y0. Compare them to the known (simulated) conditional variances.

vE = infer(Mdl,y,E0=y0); figure plot(1:100,v,"r",LineWidth=2) hold on plot(1:100,vE,"k:",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Presample E") hold off

There is a slightly reduced transient response in the early time periods.

Infer conditional variances using the set-aside presample variance, v0. Compare them to the known (simulated) conditional variances.

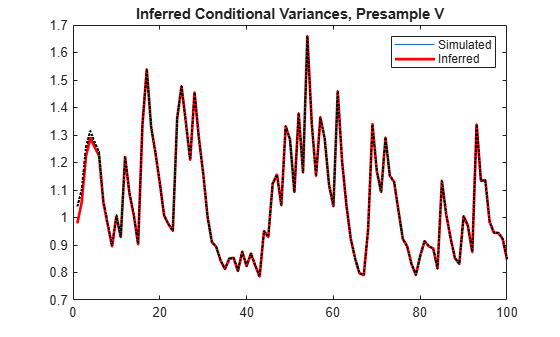

vO = infer(Mdl,y,V0=v0); figure plot(v) hold on plot(1:100,v,"r",LineWidth=2) plot(1:100,vO,"k:",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Presample V") hold off

The transient response is almost eliminated.

Infer conditional variances using both the presample innovation and conditional variance. Compare them to the known (simulated) conditional variances.

vEO = infer(Mdl,y,E0=y0,V0=v0); figure plot(v) hold on plot(1:100,v,"r",LineWidth=2) plot(1:100,vEO,"k:",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Presamples") hold off

When you use sufficient presample innovations and conditional variances, the inferred conditional variances are exact (there is no transient response).

Infer conditional variances from a GJR(1,1) model with known coefficients. When you use, and then do not use presample data, compare the results from infer.

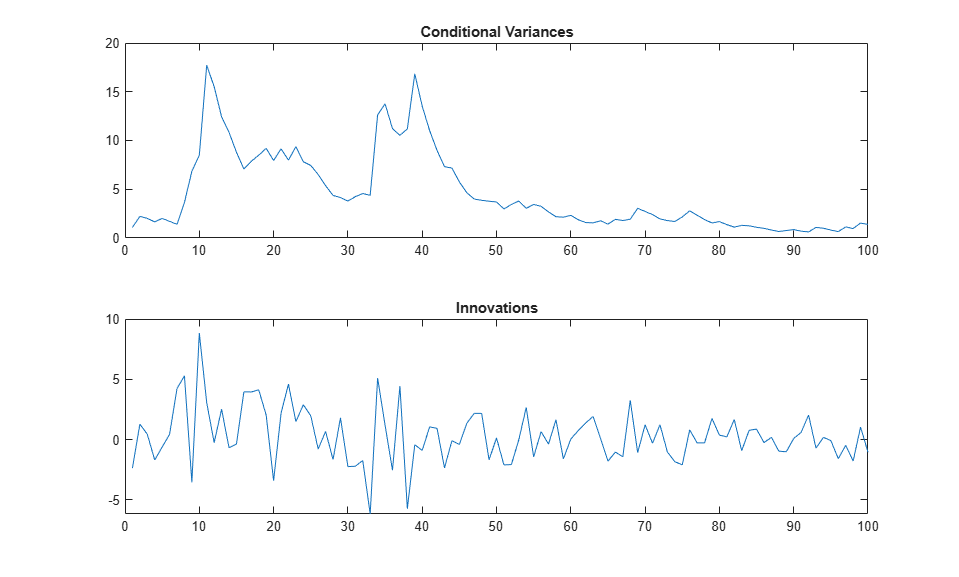

Specify a GJR(1,1) model with known parameters. Simulate 101 conditional variances and responses (innovations) from the model. Set aside the first observation from each series to use as presample data.

Mdl = gjr(Constant=0.01,GARCH=0.8,ARCH=0.14,Leverage=0.1); rng(1,"twister") % For reproducibility [vS,yS] = simulate(Mdl,101); y0 = yS(1); v0 = vS(1); y = yS(2:end); v = vS(2:end); figure tiledlayout(2,1) nexttile plot(v) title("Conditional Variances") nexttile plot(y) title("Innovations")

Infer the conditional variances of y without using any presample data. Compare them to the known (simulated) conditional variances.

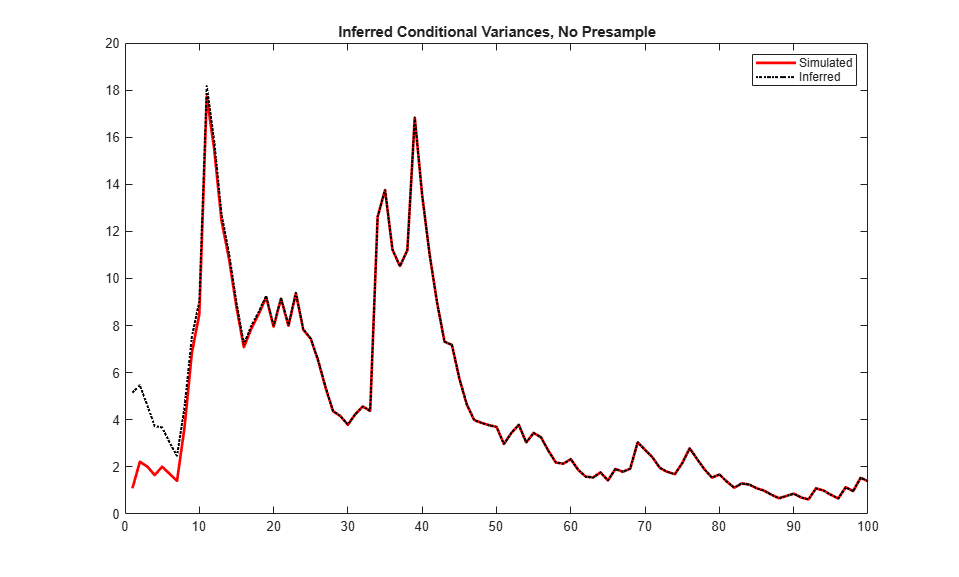

vI = infer(Mdl,y); figure plot(1:100,v,LineWidth=2) hold on plot(1:100,vI,":",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, No Presample") hold off

Notice the transient response (discrepancy) in the early time periods due to the absence of presample data.

Infer conditional variances using the set-aside presample innovation, y0. Compare them to the known (simulated) conditional variances.

vE = infer(Mdl,y,E0=y0); figure plot(1:100,v,LineWidth=2) hold on plot(1:100,vE,":",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Presample E") hold off

The provided presample innovations slightly reduces the transient response in the early time periods.

Infer conditional variances using the set-aside presample conditional variance, vO. Compare them to the known (simulated) conditional variances.

vO = infer(Mdl,y,V0=v0); figure plot(1:100,v,LineWidth=2) hold on plot(1:100,vO,":",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Presample V") hold off

The provided presample conditional variances reduces the transient response in the early time periods more than the reduction resulting from providing presample innovations.

Infer conditional variances using both the presample innovation and conditional variance. Compare them to the known (simulated) conditional variances.

vEO = infer(Mdl,y,E0=y0,V0=v0); figure plot(1:100,v,LineWidth=2) hold on plot(1:100,vEO,":",LineWidth=1.5) legend("Simulated","Inferred",Location="northeast") title("Inferred Conditional Variances, Presamples") hold off

The provided presample innovations and conditional variances reduces the transient response in the early time periods to zero.

Since R2023a

Infer the loglikelihood objective function values for an EGARCH(1,1) and EGARCH(2,1) model fit to the average weekly closing NASDAQ returns. To identify which model is the more parsimonious, adequate fit, conduct a likelihood ratio test. Specify data in timetables.

Load the U.S. equity indices data Data_EquityIdx.mat.

load Data_EquityIdxThe timetable DataTimeTable contains the daily NASDAQ closing prices, among other indices.

Compute the weekly average closing prices of all timetable variables.

DTTW = convert2weekly(DataTimeTable,Aggregation="mean");Compute the weekly returns and their sample mean.

DTTRet = price2ret(DTTW); DTTRet.Interval = []; T = height(DTTRet)

T = 626

When you plan to supply a timetable, you must ensure it has all the following characteristics:

The selected response variable is numeric and does not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the timetable, relative to the NASDAQ returns series.

DTTRet = rmmissing(DTTRet,DataVariables="NASDAQ");

numobs = height(DTTRet)numobs = 626

Because all sample times have observed NASDAQ returns, rmmissing does not remove any observations.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTTRet,"weeks")areTimestampsRegular = logical

1

areTimestampsSorted = issorted(DTTRet.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 1 indicates that the timestamps of DTTRet represent a regular weekly sample. areTimestampsSorted = 1 indicates that the timestamps are sorted.

Reserve the first two observations to use as a presample.

DTTRet0 = DTTRet(1:2,:); DTTRet = DTTRet(3:end,:);

Fit an EGARCH(1,1) model to the returns. Supply in-sample and presample data in timetables, and specify NASDAQ as the variable containing the presample innovations. Infer the loglikelihood objective function value.

MdlEGARCH11 = egarch(1,1); MdlEGARCH11.SeriesName = "NASDAQ"; EstMdlEGARCH11 = estimate(MdlEGARCH11,DTTRet, ... Presample=DTTRet0,PresampleInnovationVariable="NASDAQ");

EGARCH(1,1) Conditional Variance Model (Gaussian Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ __________

Constant -0.48899 0.15218 -3.2133 0.0013123

GARCH{1} 0.95567 0.013348 71.598 0

ARCH{1} 0.2766 0.052276 5.2912 1.2154e-07

Leverage{1} -0.10593 0.025607 -4.1366 3.5244e-05

[TblEGARCH11,logLEGARCH11] = infer(EstMdlEGARCH11,DTTRet, ... Presample=DTTRet0,PresampleInnovationVariable="NASDAQ"); tail(TblEGARCH11)

Time NYSE NASDAQ NASDAQ_Variance NASDAQ_Residual

___________ ___________ ___________ _______________ _______________

16-Nov-2001 0.0021092 0.0048052 3.4439e-05 0.0048052

23-Nov-2001 0.001451 0.00085891 3.0717e-05 0.00085891

30-Nov-2001 -0.00039051 0.0020552 2.4587e-05 0.0020552

07-Dec-2001 0.00087108 0.005263 2.0775e-05 0.005263

14-Dec-2001 -0.002694 -0.0012244 2.0067e-05 -0.0012244

21-Dec-2001 0.0019929 -0.00094985 1.7698e-05 -0.00094985

28-Dec-2001 0.0019952 -4.93e-05 1.5413e-05 -4.93e-05

04-Jan-2002 -0.00011742 -0.0012263 1.2447e-05 -0.0012263

TblEGARCH11 is a timetable of NASDAQ residuals NASDAQ_Residual and conditional variances NASDAQ_Variance, and all variables in the specified in-sample data DTTRet. logLEGARCH11 is the loglikelihood of the estimated model EstMdlEGARCH11 evaluated at the specified presample and in-sample data.

Fit an EGARCH(2,1) model to the returns. Supply in-sample and presample data in timetables, and specify NASDAQ as the variable containing the presample innovations. Infer the loglikelihood objective function value.

MdlEGARCH21 = egarch(2,1); MdlEGARCH21.SeriesName = "NASDAQ"; EstMdlEGARCH21 = estimate(MdlEGARCH21,DTTRet, ... Presample=DTTRet0,PresampleInnovationVariable="NASDAQ");

EGARCH(2,1) Conditional Variance Model (Gaussian Distribution):

Value StandardError TStatistic PValue

_________ _____________ __________ __________

Constant -0.48624 0.15764 -3.0846 0.0020386

GARCH{1} 0.96844 0.27069 3.5777 0.00034661

GARCH{2} -0.012511 0.26614 -0.047009 0.96251

ARCH{1} 0.27421 0.074046 3.7032 0.00021289

Leverage{1} -0.10486 0.035239 -2.9756 0.0029237

[TblEGARCH21,logLEGARCH21] = infer(EstMdlEGARCH21,DTTRet, ... Presample=DTTRet0,PresampleInnovationVariable="NASDAQ");

Conduct a likelihood ratio test, with the more parsimonious EGARCH(1,1) model as the null model, and the EGARCH(2,1) model as the alternative. The degree of freedom for the test is 1, because the EGARCH(2,1) model has one more parameter than the EGARCH(1,1) model (an additional GARCH term).

[h,p] = lratiotest(logLEGARCH21,logLEGARCH11,1)

h = logical

0

p = 0.9566

The null hypothesis is not rejected (h = 0). At the 0.05 significance level, the EGARCH(1,1) model is not rejected in favor of the EGARCH(2,1) model.

A GARCH(P, Q) model is nested within a GJR(P, Q) model. Therefore, you can perform a likelihood ratio test to compare GARCH(P, Q) and GJR(P, Q) model fits.

Infer the loglikelihood objective function values for a GARCH(1,1) and GJR(1,1) model fit to NASDAQ Composite Index returns. Conduct a likelihood ratio test to identify which model is the more parsimonious, adequate fit.

Load the NASDAQ data included with the toolbox, and convert the index to returns. Set aside the first two observations to use as presample data.

load Data_EquityIdx

nasdaq = DataTable.NASDAQ;

r = price2ret(nasdaq);

r0 = r(1:2);

rn = r(3:end);Fit a GARCH(1,1) model to the returns, and infer the loglikelihood objective function value.

Mdl1 = garch(1,1); EstMdl1 = estimate(Mdl1,rn,E0=r0);

GARCH(1,1) Conditional Variance Model (Gaussian Distribution):

Value StandardError TStatistic PValue

__________ _____________ __________ __________

Constant 2.0348e-06 5.4545e-07 3.7305 0.00019111

GARCH{1} 0.88275 0.008499 103.87 0

ARCH{1} 0.10956 0.0076979 14.233 5.7259e-46

[~,logL1] = infer(EstMdl1,rn,E0=r0);

Fit a GJR(1,1) model to the returns, and infer the loglikelihood objective function value.

Mdl2 = gjr(1,1); EstMdl2 = estimate(Mdl2,rn,E0=r0);

GJR(1,1) Conditional Variance Model (Gaussian Distribution):

Value StandardError TStatistic PValue

__________ _____________ __________ __________

Constant 4.4353e-06 7.1313e-07 6.2194 4.9908e-10

GARCH{1} 0.80675 0.013843 58.279 0

ARCH{1} 0.11245 0.013469 8.3488 6.8985e-17

Leverage{1} 0.11493 0.014356 8.0053 1.1914e-15

[~,logL2] = infer(EstMdl2,rn,E0=r0);

Conduct a likelihood ratio test, with the more parsimonious GARCH(1,1) model as the null model, and the GJR(1,1) model as the alternative. The degree of freedom for the test is 1, because the GJR(1,1) model has one more parameter than the GARCH(1,1) model (a leverage term).

[h,p] = lratiotest(logL2,logL1,1)

h = logical

1

p = 1.2283e-05

The null hypothesis is rejected (h = 1). At the 0.05 significance level, the GARCH(1,1) model is rejected in favor of the GJR(1,1) model.

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

If you do not specify presample data (E0 and

V0, or Presample),

infer derives the necessary presample observations from

the unconditional, or long-run, variance of the offset-adjusted response process.

For all conditional variance model types, required presample conditional variances are the sample average of the squared disturbances of the offset-adjusted specified response data (

YorTbl1).For GARCH(P,Q) and GJR(P,Q) models, the required presample innovations are the square root of the average squared value of the offset-adjusted response data.

For EGARCH(P,Q) models, the required presample innovaitons are

0.

These specifications minimize initial transient effects.

References

[1] Bollerslev, T. “Generalized Autoregressive Conditional Heteroskedasticity.” Journal of Econometrics. Vol. 31, 1986, pp. 307–327.

[2] Bollerslev, T. “A Conditionally Heteroskedastic Time Series Model for Speculative Prices and Rates of Return.” The Review of Economics and Statistics. Vol. 69, 1987, pp. 542–547.

[3] Box, G. E. P., G. M. Jenkins, and G. C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[4] Enders, W. Applied Econometric Time Series. Hoboken, NJ: John Wiley & Sons, 1995.

[5] Engle, R. F. “Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Inflation.” Econometrica. Vol. 50, 1982, pp. 987–1007.

[6] Glosten, L. R., R. Jagannathan, and D. E. Runkle. “On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks.” The Journal of Finance. Vol. 48, No. 5, 1993, pp. 1779–1801.

[7] Hamilton, J. D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.