waldtest

Wald test of model specification

Syntax

Description

h = waldtest(r,R,EstCov)

If any input argument is a cell vector of length k > 1, then the other input arguments must be cell arrays of length k.

waldtest(r,R,EstCov) treats each cell as a separate, independent test, and returns a vector of rejection decisions.If any input argument is a row vector, then the software returns output arguments as row vectors.

Examples

Check for significant lag effects in a time series regression model.

Load the U.S. GDP data set. Convert the serial dates to datetimes.

load Data_GDP dt = datetime(dates,ConvertFrom="datenum");

Plot the GDP against time.

figure plot(dt,Data)

The series seems to increase exponentially.

Transform the data using the natural logarithm.

logGDP = log(Data);

logGDP is increasing in time, so assume that there is a significant lag 1 effect. To use the Wald test to check if there is a significant lag 2 effect, you need the:

Estimated coefficients of the unrestricted model

Restriction function evaluated at the unrestricted model coefficient values

Jacobian of the restriction function evaluated at the unrestricted model coefficient values

Estimated, unrestricted parameter covariance matrix.

The unrestricted model is

Estimate the coefficients of the unrestricted model.

LagLGDP = lagmatrix(logGDP,1:2); UMdl = fitlm(table(LagLGDP(:,1),LagLGDP(:,2),logGDP));

UMdl is a fitted LinearModel model. It contains, among other things, the fitted coefficients of the unrestricted model.

The restriction is . Therefore, the restriction function (r) and Jacobian (R) are:

Specify r, R, and the estimated, unrestricted parameter covariance matrix.

r = UMdl.Coefficients.Estimate(3); R = [0 0 1]; EstParamCov = UMdl.CoefficientCovariance;

Test for a significant lag 2 effect using the Wald test.

[h,pValue] = waldtest(r,R,EstParamCov)

h = logical

1

pValue = 1.2521e-07

h = 1 indicates that the null, restricted hypothesis () should be rejected in favor of the alternative, unrestricted hypothesis. pValue is quite small, which suggests that there is strong evidence for this result.

Test whether there are significant ARCH effects in a simulated response series using waldtest.

Suppose that the model for the simulated data is AR(1) with an ARCH(1) variance. Symbolically, the model is

where

is Gaussian with mean 0 and variance 1.

Specify the model for the simulated data.

VarMdl = garch('ARCH',0.5,'Constant',1); Mdl = arima('Constant',0,'Variance',VarMdl,'AR',0.9);

Mdl is a fully specified AR(1) model with an ARCH(1) variance.

Simulate presample and effective sample responses from Mdl.

T = 100; rng(1); % For reproducibility n = 2; % Number of presample observations required for the Jacobian [y,epsilon,condVariance] = simulate(Mdl,T + n); psI = 1:n; % Presample indices esI = (n + 1):(T + n); % Estimation sample indices

epsilon is the random path of innovations from VarMdl. The software filters epsilon through Mdl to yield the random response path y.

Specify the unrestricted model assuming that the conditional mean model is

where . Fit the simulated data (y) to the unrestricted model using the presample observations.

UVarMdl = garch(0,1); UMdl = arima('ARLags',1,'Variance',UVarMdl); [UEstMdl,UEstParamCov] = estimate(UMdl,y(esI),'Y0',y(psI),... 'E0',epsilon(psI),'V0',condVariance(psI),'Display','off');

UEstMdl is the fitted, unrestricted model, and UEstParamCov is the estimated parameter covariance of the unrestricted model parameters.

The null hypothesis is that , i.e., the restricted model is AR(1) with Gaussian innovations that have mean 0 and constant variance. Therefore, the restriction function is , where . The components of the Wald test are:

The restriction function evaluated at the unrestricted parameter estimates is .

The Jacobian of r evaluated at the unrestricted model parameters is .

The unrestricted model estimated parameter covariance matrix is

UEstParamCov.

Specify r and R.

r = UEstMdl.Variance.ARCH{1};

R = [0, 0, 0, 1];Test the null hypothesis that at the 1% significance level using waldtest.

[h,pValue,stat,cValue] = waldtest(r,R,UEstParamCov,0.01)

h = logical

0

pValue = 0.0549

stat = 3.6846

cValue = 6.6349

h = 0 indicates that the null, restricted model should not be rejected in favor of the alternative, unrestricted model. This result is consistent with the model for the simulated data.

Assess model specifications by testing down among multiple restricted models using simulated data. The true model is the ARMA(2,1)

where is Gaussian with mean 0 and variance 1.

Specify the true ARMA(2,1) model, and simulate 100 response values.

TrueMdl = arima('AR',{0.9,-0.5},'MA',0.7,... 'Constant',3,'Variance',1); T = 100; rng(1); % For reproducibility y = simulate(TrueMdl,T);

Specify the unrestricted model and the names of the candidate models for testing down.

UMdl = arima(2,0,2);

RMdlNames = {'ARMA(2,1)','AR(2)','ARMA(1,2)','ARMA(1,1)',...

'AR(1)','MA(2)','MA(1)'};UMdl is the unrestricted, ARMA(2,2) model. RMdlNames is a cell array of strings containing the names of the restricted models.

Fit the unrestricted model to the simulated data.

[UEstMdl,UEstParamCov] = estimate(UMdl,y,'Display','off');

UEstMdl is the fitted, unrestricted model, and UEstParamCov is the estimated parameter covariance matrix.

The unrestricted model has six parameters. To construct the restriction function and its Jacobian, you must know the order of the parameters in UEstParamCov. For this arima model, the order is .

Each candidate model corresponds to a restriction function. Put the restriction function vectors into separate cells of a cell vector.

rf1 = UEstMdl.MA{2}; % ARMA(2,1)

rf2 = cell2mat(UEstMdl.MA)'; % AR(2)

rf3 = UEstMdl.AR{2}; % ARMA(1,2)

rf4 = [UEstMdl.AR{2};UEstMdl.MA{2}]'; % ARMA(1,1)

rf5 = [UEstMdl.AR{2};cell2mat(UEstMdl.MA)']; % AR(1)

rf6 = cell2mat(UEstMdl.AR)'; % MA(2)

rf7 = [cell2mat(UEstMdl.AR)';UEstMdl.MA{2}]; % MA(1)

r = {rf1;rf2;rf3;rf4;rf5;rf6;rf7};r is a 7-by-1 cell vector of vectors corresponding to the restriction function for the candidate models.

Put the Jacobian of each restriction function into separate, corresponding cells of a cell vector. The order of the elements in the Jacobian must correspond to the order of the elements in UEstParamCov.

J1 = [0 0 0 0 1 0]; % ARMA(2,1) J2 = [0 0 0 1 0 0; 0 0 0 0 1 0]; % AR(2) J3 = [0 1 0 0 0 0]; % ARMA(1,2) J4 = [0 1 0 0 0 0; 0 0 0 0 1 0]; % ARMA(1,1) J5 = [0 1 0 0 0 0; 0 0 0 1 0 0; 0 0 0 0 1 0]; % AR(1) J6 = [1 0 0 0 0 0; 0 1 0 0 0 0]; % MA(2) J7 = [1 0 0 0 0 0; 0 1 0 0 0 0; 0 0 0 0 1 0]; % MA(1) R = {J1;J2;J3;J4;J5;J6;J7};

R is a 7-by-1 cell vector of vectors corresponding to the restriction function for the candidate models.

Put the estimated parameter covariance matrix in each cell of a 7-by-1 cell vector.

EstCov = cell(7,1); % Preallocate for j = 1:length(EstCov) EstCov{j} = UEstParamCov; end

Apply the Wald test at a 1% significance level to find the appropriate, restricted model specifications.

alpha = .01; h = waldtest(r,R,EstCov,alpha); RestrictedModels = RMdlNames(~h)

RestrictedModels = 1×5 cell

{'ARMA(2,1)'} {'ARMA(1,2)'} {'ARMA(1,1)'} {'MA(2)'} {'MA(1)'}

RestrictedModels lists the most appropriate restricted models.

You can test down again, but use ARMA(2,1) as the unrestricted model. In this case, you must remove MA(2) from the possible restricted models.

Test whether the parameters of a nested model have a nonlinear relationship.

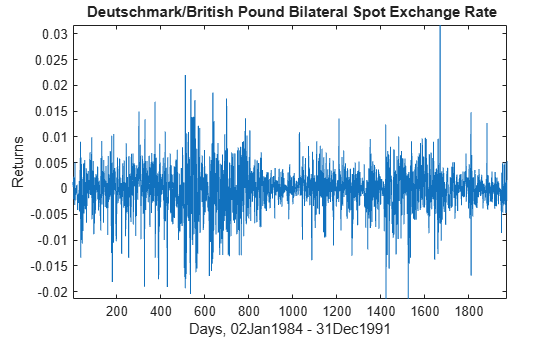

Load the Deutschmark/British Pound bilateral spot exchange rate data set.

load Data_MarkPoundThe data set (Data) contains a time series of prices.

Convert the prices to returns, and plot the return series.

returns = price2ret(Data); figure plot(returns) axis tight ylabel('Returns') xlabel('Days, 02Jan1984 - 31Dec1991') title('{\bf Deutschmark/British Pound Bilateral Spot Exchange Rate}')

The returns series shows signs of heteroscedasticity.

Suppose that a GARCH(1,1) model is an appropriate model for the data. Fit a GARCH(1,1) model to the data including a constant.

Mdl = garch(1,1); [EstMdl,EstParamCov] = estimate(Mdl,returns);

GARCH(1,1) Conditional Variance Model (Gaussian Distribution):

Value StandardError TStatistic PValue

__________ _____________ __________ __________

Constant 1.0876e-06 3.5504e-07 3.0634 0.0021883

GARCH{1} 0.80425 0.013154 61.139 0

ARCH{1} 0.15468 0.011637 13.292 2.5766e-40

g1 = EstMdl.GARCH{1};

a1 = EstMdl.ARCH{1};g1 is the estimated GARCH effect, and a1 is the estimated ARCH effect.

The following might represent relationships between the GARCH and ARCH coefficients:

where is the GARCH effect and is the ARCH effect. Specify these relationships as the restriction function , evaluated at the unrestricted model parameter estimates. This specification defines a nested, restricted model.

r = [g1*a1; g1+a1] - 1;

Specify the Jacobian of the restriction function vector.

R = [0, a1, g1;0, 1, 1];

Conduct a Wald test to assess whether there is sufficient evidence to reject the restricted model.

[h,pValue,stat,cValue] = waldtest(r,R,EstParamCov)

h = logical

1

pValue = 0

stat = 1.4419e+04

cValue = 5.9915

h = 1 indicates that there is sufficient evidence to reject the restricted model in favor of the unrestricted model. pValue = 0 indicates that the evidence for rejecting the restricted model is strong.

Input Arguments

Output Arguments

More About

Tips

Estimate unrestricted univariate linear time series models, such as

arimaorgarch, or time series regression models (regARIMA) usingestimate. Estimate unrestricted multivariate linear time series models, such asvarmorvecm, usingestimate.estimatereturns parameter estimates and their covariance estimates, which you can process and use as inputs towaldtest.If you cannot easily compute restricted parameter estimates, then use

waldtest. By comparison:lratiotestrequires both restricted and unrestricted parameter estimates.lmtestrequires restricted parameter estimates.

Algorithms

waldtestperforms multiple, independent tests when the restriction function vector, its Jacobian, and the unrestricted model parameter covariance matrix (r,R, andEstCov, respectively) are equal-length cell vectors.If

EstCovis the same for all tests, butrvaries, thenwaldtest“tests down” against multiple restricted models.If

EstCovvaries among tests, butrdoes not, thenwaldtest“tests up” against multiple unrestricted models.Otherwise,

waldtestcompares model specifications pair-wise.

alphais nominal in that it specifies a rejection probability in the asymptotic distribution. The actual rejection probability is generally greater than the nominal significance.The Wald test rejection error is generally greater than the likelihood ratio and Lagrange multiplier test rejection errors.

References

[1] Davidson, R. and J. G. MacKinnon. Econometric Theory and Methods. Oxford, UK: Oxford University Press, 2004.

[2] Godfrey, L. G. Misspecification Tests in Econometrics. Cambridge, UK: Cambridge University Press, 1997.

[3] Greene, W. H. Econometric Analysis. 6th ed. Upper Saddle River, NJ: Pearson Prentice Hall, 2008.

[4] Hamilton, J. D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

Version History

Introduced in R2009a