corr

Model-implied temporal correlations of state-space model

Syntax

Description

The corr function returns model-implied temporal correlations and covariances of the state or measurement variables in a stationary, time-invariant state-space model. To determine whether the model captures characteristics present in the data, You can compare model-implied associations of present and lagged variables to sample analogues. Other state-space model tools to characterize the dynamics of a specified system include the following:

The impulse response function (IRF), computed by

irfand plotted byirfplot, traces the effects of a shock to a state disturbance on the measurement variables in the system.The forecast error variance decomposition (FEVD), computed by

fevd, provides information about the relative importance of each state disturbance in affecting the forecast error variance of all measurement variables in the system.

Fully Specified State-Space Model

Cyy = corr(Mdl,Name,Value)'Covariance',true,'NumLags',10 specifies returning temporal covariances Cov(yt,yt – h), h = 0 through 10.

[ also returns Corr(xt,xt – h), the correlations between the state variables and their self-lags Cyy,Cxx,Cyx] = corr(___)Cxx, and Corr(yt,xt – h), the correlations between the state variables and their self lags Cxx and the cross-correlations between the measurement variables and lags of the state variables Cyx using any of the input argument combinations in the previous syntaxes. h is the value of the NumLags name-value argument. corr returns covariances when the value of the Covariance name-value argument is true.

Examples

Explicitly create the state-space model

A = [0.9 0; 0.1 0.3];

B = [0.2 0; 0 1];

C = [1 0; 1 1];

Mdl = ssm(A,B,C,'StateType',[0 0])Mdl =

State-space model type: ssm

State vector length: 2

Observation vector length: 2

State disturbance vector length: 2

Observation innovation vector length: 0

Sample size supported by model: Unlimited

State variables: x1, x2,...

State disturbances: u1, u2,...

Observation series: y1, y2,...

Observation innovations: e1, e2,...

State equations:

x1(t) = (0.90)x1(t-1) + (0.20)u1(t)

x2(t) = (0.10)x1(t-1) + (0.30)x2(t-1) + u2(t)

Observation equations:

y1(t) = x1(t)

y2(t) = x1(t) + x2(t)

Initial state distribution:

Initial state means

x1 x2

0 0

Initial state covariance matrix

x1 x2

x1 0.21 0.03

x2 0.03 1.10

State types

x1 x2

Stationary Stationary

Mdl is an ssm model object. Because all parameters have known values, the object is fully specified.

Compute the temporal correlations of the measurement variables through lag 1.

Cyy = corr(Mdl)

Cyy =

Cyy(:,:,1) =

1.0000 0.4411

0.9000 0.4072

Cyy(:,:,2) =

0.4411 1.0000

0.3970 0.4212

Rows correspond to lags, columns correspond to the latest observation of the measurement variable in the correlation, and pages correspond to the lagged measurement variable. For example, is 0.3970.

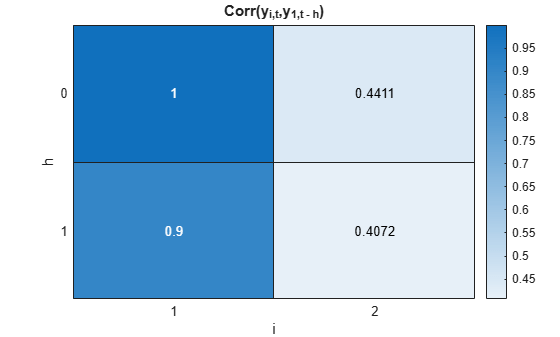

Display a heatmap of the temporal correlations between the latest observation of each measurement variable and all lags of measurement variable 1.

Corryy1 = Cyy(:,:,1); hm = heatmap(Corryy1); ylabel('h'); hm.YDisplayLabels = ["0" "1"]; xlabel('i') hm.XDisplayLabels = ["1" "2"]; title('Corr(y_{i,t},y_{1,t - h})')

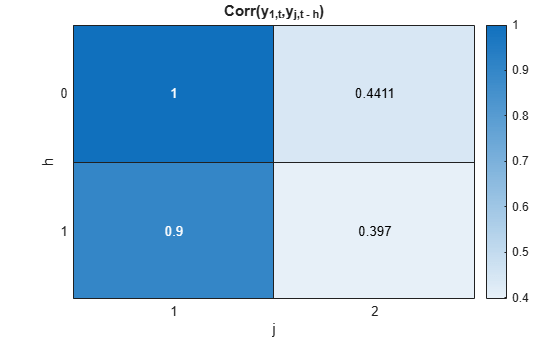

Display a heatmap of the temporal correlations between the current observation of measurement variable 1 and all lags of all measurement variables.

Corry1y = squeeze(Cyy(:,1,:)); hm = heatmap(Corry1y); ylabel('h'); hm.YDisplayLabels = ["0" "1"]; xlabel('j') hm.XDisplayLabels = ["1" "2"]; title('Corr(y_{1,t},y_{j,t - h})')

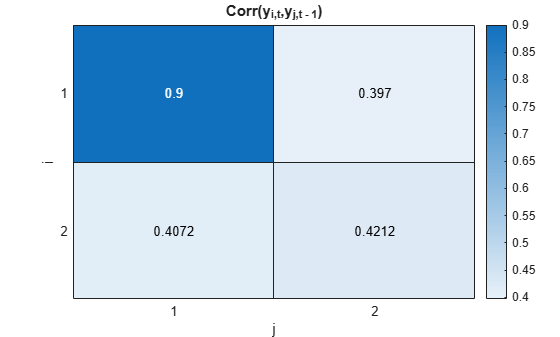

Display a heatmap of the temporal correlations between the current observation of all measurement variables and the first lag of all measurement variables.

Corryylag1 = squeeze(Cyy(2,:,:)); hm = heatmap(Corryylag1); ylabel('i'); hm.YDisplayLabels = ["1" "2"]; xlabel('j') hm.XDisplayLabels = ["1" "2"]; title('Corr(y_{i,t},y_{j,t - 1})')

Explicitly create the state-space model

A = [0.9 0; 0.1 -0.3];

B = [0.2 0; 0 1];

C = [1 0; 1 1];

D = eye(2);

Mdl = ssm(A,B,C,D,'StateType',[0 0]);Mdl is an ssm model object.

Compute the temporal correlations of the measurement variables from lag 0 through 20.

numlags = 20;

Cyy = corr(Mdl,'NumLags',numlags);Cyy is a 21-by-2-by-2 array representing the 20-period temporal correlations of the measurement variables.

Display Cyy(:,2,2), which is the model-implied autocorrelation of .

acfy2 = Cyy(:,2,2)

acfy2 = 21×1

1.0000

-0.0466

0.1267

0.0634

0.0723

0.0605

0.0558

0.0498

0.0449

0.0404

0.0364

0.0327

0.0295

0.0265

0.0239

⋮

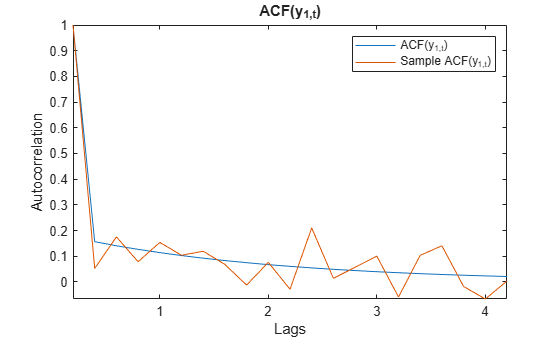

Generate a random path of measurements of length 200 from the model.

rng(1); % For reproducibility

Y = simulate(Mdl,200);Compute the sample autocorrelation function (ACF) of each variable for 2q0 lags.

sacfy1 = autocorr(Y(:,1),'NumLags',numlags); sacfy2 = autocorr(Y(:,2),'NumLags',numlags);

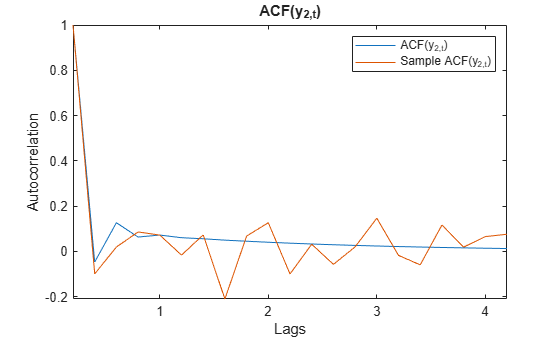

Visually compare the model-implied and sample ACF of each measurement variable.

acfy1 = Cyy(:,1,1); plot([acfy1 sacfy1]) xticklabels(0:numlags) ylabel("Autocorrelation") xlabel("Lags") legend(["ACF(y_{1,t})" "Sample ACF(y_{1,t})"]) title("ACF(y_{1,t})") axis tight

plot([acfy2 sacfy2]) xticklabels(0:numlags) ylabel("Autocorrelation") xlabel("Lags") legend(["ACF(y_{2,t})" "Sample ACF(y_{2,t})"]) title("ACF(y_{2,t})") axis tight

Explicitly create the state-space model

A = [0.9 0; 0.1 -0.3];

B = [0.2 0; 0 1];

C = [1 0; 1 1];

D = eye(2);

Mdl = ssm(A,B,C,D,'StateType',[0 0]);Mdl is an ssm model object.

Compute the temporal correlations of the measurement and state variables, as well as their cross-correlations.

[Cyy,Cxx,Cyx] = corr(Mdl);

Each output variable is a 2-by-2-by-2 array containing temporal correlations from lag 0 to 1. Cyy contains the correlations between the measurement variables, Cxx contains the correlations among the state variables, and Cyx contains cross-correlations between the current observation of the measurement variables and lagged state variables.

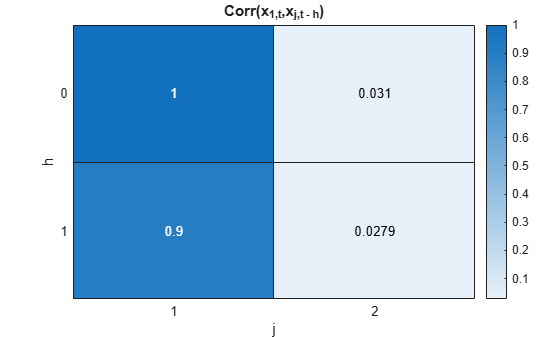

Plot a heatmap of the correlations between and the lags of all state variables.

Cx1x = squeeze(Cxx(:,1,:)); hm = heatmap(Cx1x); ylabel('h'); hm.YDisplayLabels = ["0" "1"]; xlabel('j') hm.XDisplayLabels = ["1" "2"]; title('Corr(x_{1,t},x_{j,t - h})')

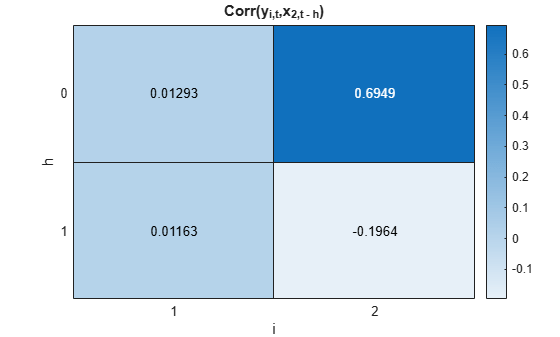

Plot a heatmap of the cross-correlations between all measurement variables and the lags of .

Cyx2 = Cyx(:,:,2); hm = heatmap(Cyx2); ylabel('h'); hm.YDisplayLabels = ["0" "1"]; xlabel('i') hm.XDisplayLabels = ["1" "2"]; title('Corr(y_{i,t},x_{2,t - h})')

Simulate data from a known model, fit a model to the data, and then compare sample and model-implied covariances.

Simulate Data

Explicitly create the state-space model

ADGP = [0.9 0; 0.1 -0.3];

BDGP = [0.2 0; 0 1];

CDGP = [1 0; 1 1];

DDGP = eye(2);

DGP = ssm(ADGP,BDGP,CDGP,DDGP,'StateType',[0 0]);Generate a random path of measurements of length 500 from the model.

rng(1); % For reproducibility

numobs = 500;

Y = simulate(DGP,numobs);Fit Model to Data

Create a state-space model template to fit to the data by replacing each nonzero state parameter of the data-generating process with a NaN value.

A = [NaN 0; NaN NaN];

B = [NaN 0; 0 NaN];

Mdl = ssm(A,B,CDGP,DDGP,'StateType',[0 0]);Fit the model template to the data. Specify a random set of positive starting values. Return the vector of estimated parameters.

[~,estParams] = estimate(Mdl,Y,abs(rand(5,1)));

Method: Maximum likelihood (fminunc)

Sample size: 500

Logarithmic likelihood: -1694.08

Akaike info criterion: 3398.15

Bayesian info criterion: 3419.23

| Coeff Std Err t Stat Prob

---------------------------------------------------

c(1) | 0.91506 0.04229 21.63956 0

c(2) | -0.25898 0.25406 -1.01934 0.30805

c(3) | -0.15383 0.08243 -1.86621 0.06201

c(4) | -0.16808 0.04926 -3.41221 0.00064

c(5) | 1.19275 0.06842 17.43153 0

|

| Final State Std Dev t Stat Prob

x(1) | -0.12293 0.30568 -0.40217 0.68756

x(2) | -0.80608 0.79263 -1.01697 0.30917

Compute Covariances

Compute model-implied temporal covariances of the measurement variables by passing the state-space model template and estimated parameters to corr. Return the covariances instead of the correlations.

Covyy = corr(Mdl,'Params',estParams,'Covariance',true)

Covyy =

Covyy(:,:,1) =

1.1737 0.1376

0.1589 0.1195

Covyy(:,:,2) =

0.1376 2.5676

0.1259 -0.1297

Covyy is a 2-by-2-by-2 array of temporal covariances of the measurement variables.

Compute the sample covariances of the measurement variables and their first lags.

AugData = lagmatrix(Y,[0 1]); SCovyy = cov(AugData(2:end,:));

Compare Covariances

Compare the model-implied temporal covariances and the sample covariances.

names = ["y_1t" "y_2t" "y_1t-1" "y_2t-1"]; Covy1y = squeeze(Covyy(:,1,:))'; Covy2y = squeeze(Covyy(:,2,:))'; CovyLag1 = [Covy1y(:,2) Covy2y(:,2) Covy1y(:,1) Covy2y(:,1)]'; ModelCovariances = array2table([Covy1y(:) Covy2y(:) CovyLag1],'RowNames',names,... 'VariableNames',names)

ModelCovariances=4×4 table

y_1t y_2t y_1t-1 y_2t-1

_______ ________ _______ ________

y_1t 1.1737 0.13759 0.15891 0.1259

y_2t 0.13759 2.5676 0.11949 -0.12972

y_1t-1 0.15891 0.11949 1.1737 0.13759

y_2t-1 0.1259 -0.12972 0.13759 2.5676

SampleCovariances = array2table(SCovyy,'RowNames',names,'VariableNames',names)

SampleCovariances=4×4 table

y_1t y_2t y_1t-1 y_2t-1

________ ________ ________ ________

y_1t 1.2459 0.22058 0.11689 0.070475

y_2t 0.22058 2.5332 0.074687 -0.17466

y_1t-1 0.11689 0.074687 1.2437 0.22158

y_2t-1 0.070475 -0.17466 0.22158 2.5419

The model-implied and sample covariances appear to be similar in magnitude. Note that the covariances are invariant to the reference time; for example, Cov() = Cov().

Input Arguments

Name-Value Arguments

Output Arguments

More About

Tips

To obtain an association matrix of lead variables from an association matrix of lagged variables, use the identity

where:

C is an association function, either Corr or Cov.

at and bt are yt or xt.

Version History

Introduced in R2021a